Durkin Law PC

Successful narrative appraisal report writing is based in the recognition that the appraisal report is an argument. An argument is a set of assertions supported by logic and evidence. According to USPAP and Black’s Law Dictionary, the term credible means worthy of belief. USPAP states that credible assignment results require support by relevant evidence and logic. The process is clear. The report is not a theme paper, not an estimate, and not an essay. The appraisal report is an argument supporting your professional opinion about the economic exchange value of the rights inherent in the ownership of property.

Most appraisers, especially those who have decades of experience, think their appraisals are faultless. The appraiser claims the appraisals were performed in accordance with USPAP or the Appraisal Institute, or AICPA Standards, or a mixture of two or three appraisal association guidelines. Appraisers need to question their reliance on old appraisal dogma. Appraisers abhor appraisal criticism and especially reject criticism of their use of dogma. Dogma is part historical creed, habitual belief, and behavior doctrine imposed by trade associations as a code of performance. I strongly suggest that you stop being trapped by dogma. Some dogma is un-evolved archaic faith-based methodology. Dogma includes archaic trade terms such as function which means purpose and “purpose” which means resolve and appraisal problem which means enigma or puzzle. You may be steeped in this word-stew and think you know what the words mean. Your client may not. The appraiser wrote, “the problem to be solved in this appraisal is to estimate the market value of the leased fee interest in the property as is.” For 50-years appraisers have tried to identify the “problem” when in reality appraisal work is not a problem to be solved, it is an issue to be addressed, a question to be answered, or an intended use to be explained. USPAP dropped function, purpose and estimate of value about 12-years ago. Yet, the dogma continues. The term “problem” and “estimate” was replaced with intended use and opinion of value. An appraiser is required to identify the interest to be appraised. Leased-fee interest is not a real property legal interest. The term leased fee is appraisal jargon. The Appraisal Institute dictionary is not an authoritative source for defining a legal interest. Leased-Fee is not a fee interest. Leased-Fee is a tenancy-for-a-term. AS IS means present existing conditions to prospective buyers. Then why do appraisers say it is AS IS and then forecast fictitious income and expenses while ignoring the present physical and economic condition?

Dogma is living with results of other appraisers’ historical appraisal practice thinking. Habitual thinking is passed down to you and internalized. It becomes your dogma. Think about the many methodology myths in appraisal. Maybe some of the valuation theories and appraisal methods you hold as sacrosanct are not reasonable, are common-sensical, and not logically valid. Dogma-decrees include; (1) there are three approaches to value! And only three. The three approaches are set in stone, mandated and considered al holy trinity. According to USPAP, you must consider all three approaches in every discipline whether appraising real estate, an antique chair, a business, a painting, a diamond ring, or a trademark. How does one apply an income approach to an antique chair? Do we pretend hypothetically to rent the chair? Who rents antique chairs? (2) Dogma-decreed and USPAP adopted that highest and best use analysis be applied to personal property. This requirement stayed in USPAP Standard 8 for seven years. Eventually, ASB was dropped it. (3) Dogma commanded that cap rates be based on PWC Korpacz Real Estate Investor Survey. Dogma now decrees that cap rates be based on what Coldwell Banker North American Cap Rate Report. The problem with this is relevancy. Korpacz and CBRE obtain data from large publicly traded real estate  trusts whose detail financial operations are public. The great majority of commercial real estate does not disclose operating expenses or net income. (4) Dogma of adjustments is based on subjective guesses. (5) Dogma teaches that DCF method can use a forecasted Single Period Capitalization method that magically capitalizes one year’s forecast of “market derived” revenue and expenses. (6) DCF forecasting using Argus Valuation Life Version software is based on nothing more than the “appraiser’s belief” or inflation or made up “stabilized” expenses is at best voodoo mathematics.

trusts whose detail financial operations are public. The great majority of commercial real estate does not disclose operating expenses or net income. (4) Dogma of adjustments is based on subjective guesses. (5) Dogma teaches that DCF method can use a forecasted Single Period Capitalization method that magically capitalizes one year’s forecast of “market derived” revenue and expenses. (6) DCF forecasting using Argus Valuation Life Version software is based on nothing more than the “appraiser’s belief” or inflation or made up “stabilized” expenses is at best voodoo mathematics.

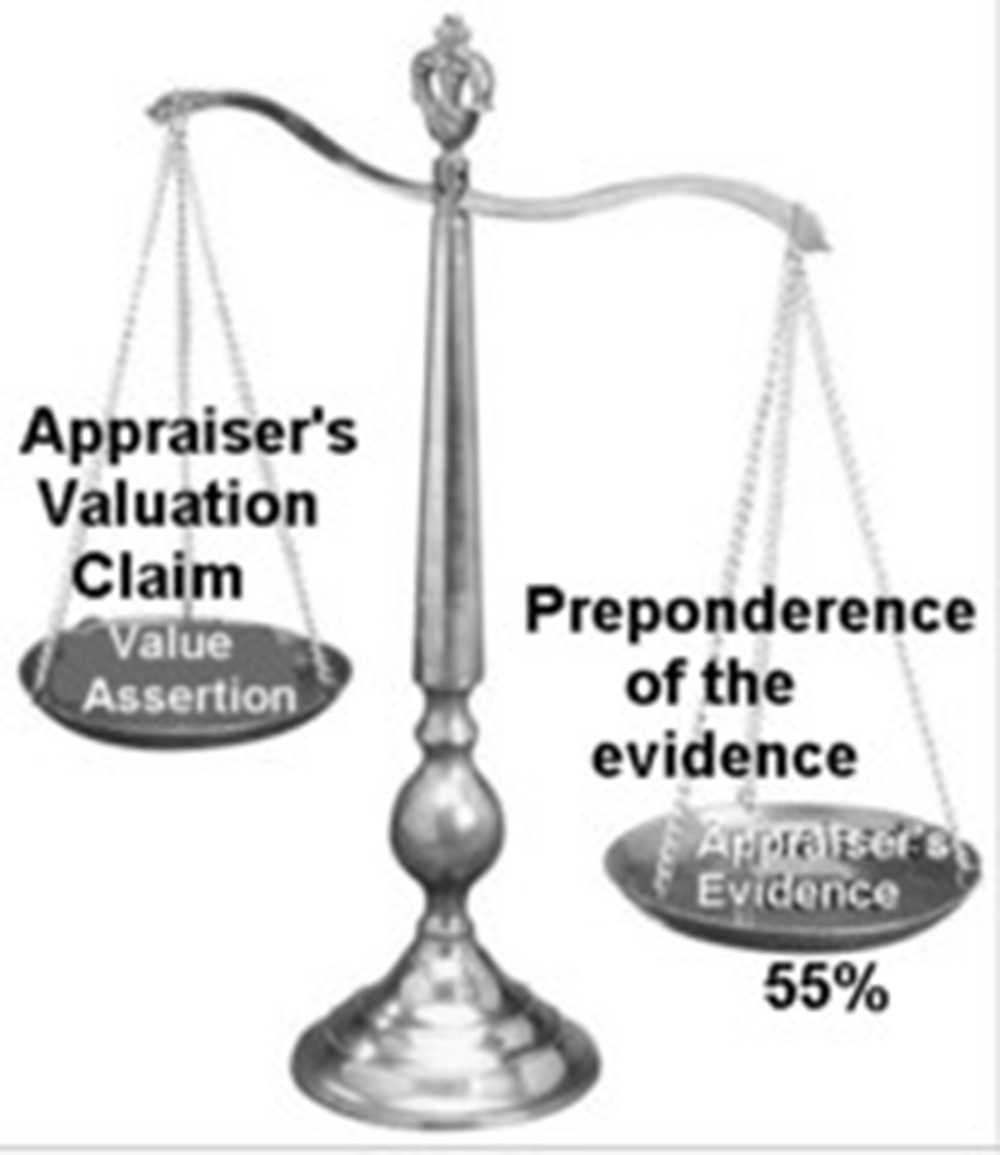

An appraisal is a professional opinion relative to the defined economic exchange value of the rights inherent in the ownership of property supported by a preponderance of the evidence. Evidence is something that tends to prove or disprove the existence of an alleged fact. The scale is tilted 51% more likely true than not true. Evidence that is sufficient must be also be credible, relevant, and material. Credible evidence is that evidence worthy of belief. Black’s Law defines substantial evidence as “evidence that a reasonable mind would accept as adequate to support a conclusion, evidence beyond a scintilla.”

The iPhone was a collection of existing technologies put together in a new way. Appraisers will need to rethink and question existing dogma. Appraisers need to develop new data analysis skill sets. There is a rapid rise of non-traditional sources of data and predictive analysis. The appraisal profession is evolving with the possibilities of big-data, statistical and predictive analysis and the magic of applied artificial intelligence. Fannie Mae is moving beyond the theoretical stage by implemented big-data analysis and valuation algorithms. All of which will dramatically change the role of appraisers.

Roger Durkin, JD, MS, FASA is an attorney with Durkin Law PC, Boston, Mass.