The Boston and Cambridge lodging market prepares for an eventful, but measured, year ahead - by Sebastian Colella

The Boston and Cambridge lodging market has a lot to look forward to in 2026. As one of eleven host cities for the FIFA World Cup, the focal point of the nation’s 250th anniversary celebrations, and the beneficiary of a few well-timed citywide events, the region is poised for an exciting year ahead. Even when considering a macro economic landscape with greater clarity than last year, and positive year-over-year comparisons to a soft 2025, the near-term outlook remains relatively steady, with growth expectations measured, rather than high.

2025: A Year of Deceleration

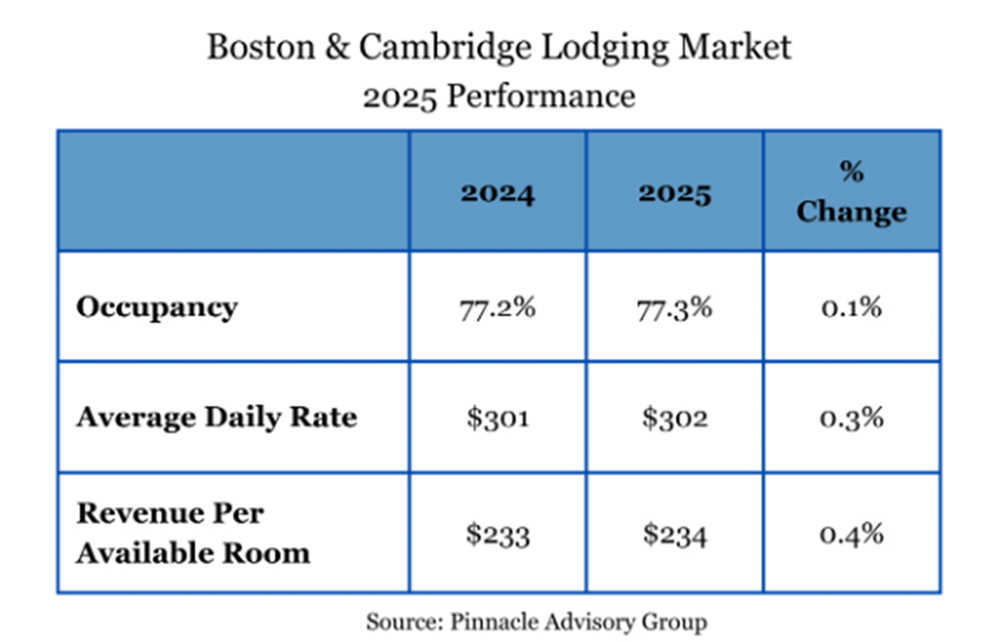

Demand growth in the Boston & Cambridge lodging market slowed to 0.4% in 2025. Broader macro headwinds, including government spending cutbacks, uncertainty around tariffs, a slowdown in inbound international travel, and the eventual government shutdown in Q4, were felt locally across all demand segments.

Shortly after the market benefited from the Biotechnology Innovation Organization International Convention in June, group demand declined through July and August to a point that limited pricing power during the peak summer season. As a result, ADR declined for three of the markets most critical months. On an annual basis, ADR increased just 0.3% in 2025, presenting a downward trend given the growth was 4.8% and 3.0% in 2023 and 2024 respectively.

With occupancy largely flat, RevPAR rose a modest 0.4% in 2025. Similar to trends seen nationally, RevPAR growth was uneven across hotel scales. While the nine luxury hotels, as defined by Pinnacle Advisory Group, experienced a RevPAR increase of almost 10%, three of the four middle and lower tier segments experienced declines. (See Chart 1)

Signature Events in 2026 as Targeted Demand Drivers

Boston’s role as a host city for the 2026 FIFA World Cup introduces a meaningful, though highly concentrated, demand catalyst. With seven match dates in June and July, months when the market historically operates at or above 85% occupancy, the net annual benefit is expected to be largely rate driven.

It is still early in the booking cycle, however preliminary patterns suggest a cautious approach by individual travelers, groups, and organizers alike. Hoteliers have expressed concerns around travel visas, geopolitical uncertainty, ticket pricing, distance from Boston, and the role of alternative accommodations such as Airbnb, a major event sponsor. Even so, global events of this scale matter for a market like Boston, not only for near-term performance, but for long-term visibility, international awareness, and future travel demand.

Not to be forgotten, it’s the nation’s 250th anniversary which presents an additional, and potentially meaningful, opportunity. As the birthplace of the American story, Greater Boston stands to benefit disproportionately if programming is executed effectively. Combined with July Fourth celebrations, the Tall Ships returning in mid-July, and the region’s existing cultural attractions, the anniversary could provide incremental lodging demand shortly after Boston’s last quarterfinal match.

A Slow and Steady 2026

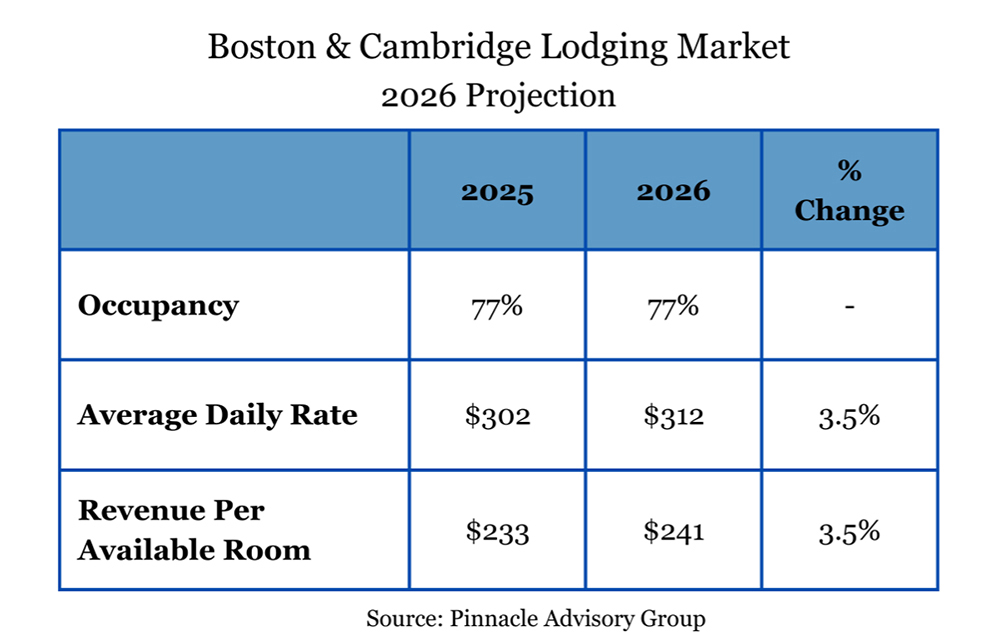

Pinnacle Advisory Group has projected the Boston & Cambridge lodging market demand to increase 1.0%, a considerable increase from last year. New supply will be limited to just two hotel openings, the 246-room Atlas Hotel at Harvard’s Enterprise Research Campus and the 123-room Cambria East Boston, keeping overall inventory growth to a modest 1.0%. Offsetting potential demand growth in 2026 is a weaker convention calendar, particularly in the first half of the year, continued softness in inbound international travel, and several unfavorable calendar shifts, such as the timing of Easter and the Boston Marathon and a late Labor Day. As a result, market occupancy is projected to hold steady at 77% for a third consecutive year, reinforcing the view that future performance gains will be driven less by volume and more by average daily rate.

Average daily rate is projected to increase 3.5% in 2026, supported by high-profile demand drivers including the FIFA World Cup, which is expected to generate concentrated, rate-driven lift around match dates, particularly in June and July. That said, broader growth will be tempered by a softer convention calendar and less favorable date patterns for certain holidays and events, limiting compression outside of peak periods. With occupancy flat, and pricing power uneven by month, RevPAR growth is likewise projected at 3.5%. (See Chart 2)

The 2026 calendar year is shaping up to be a year defined by stabilization rather than acceleration. With supply growth limited, occupancy steady, and ADR projected to see the beginning of a rebound, the Boston & Cambridge lodging market is expected to post moderate, rate-driven gains. The signature events will provide moments of high performance, but the broader story is one of measured growth and a market rebuilding momentum following a soft 2025.

Sebastian Colella is the managing principal of Pinnacle Advisory Group, a Boston-based hospitality consulting firm with more than three decades of industry experience. With over 25 years in hospitality, including more than a decade at Pinnacle, Colella’s background spans hotel operations, acquisitions, development, and asset management across major U.S. markets and resort destinations. He has held roles with leading hospitality brands, including The Ritz-Carlton, ClubCorp (now Invited), and Rosewood Hotels & Resorts. Colella currently serves on the Board of the Massachusetts Lodging Association. He attended Cornell University’s School of Hotel Administration.