News:

Spotlight Content

Posted: May 31, 2019

What happens to your company’s flood insurance if the flood zone changes? - by Frank Licata

Licata Risk & Insurance Advisors

Coverage can be here today and gone tomorrow!

Sea levels are rising; rainfall is increasing; and flood zones are changing.

Do you know what affect the latter has on your company’s flood insurance?

We buy property insurance on a particular property for a particular policy term and we expect that, at least until the end of the policy term, coverage will remain in effect on that property. There is some cynical behavior by the insurance industry with flood insurance however, that makes that scenario not so certain anymore.

In the commercial market there are private flood insurance insurers operating in addition to the coverage provided by FEMA. The private insurers supplement the low limits offered by FEMA, or replace FEMA altogether in the low hazard flood zones.

How Flood Zones Work

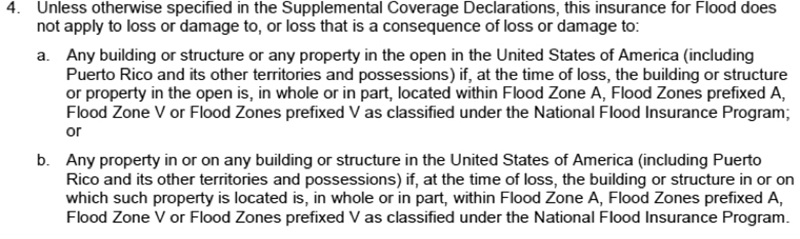

Virtually every property in the country is in a specific flood zone established by FEMA. The zones are:

--- High hazard: A, V

--- Moderate hazard: B, shaded X

--- Minimal hazard: C, X

The commercial flood insurance market operates generally like this:

In high hazard areas (A, V) they will provide coverage only excess of FEMA’s maximum limit which is either $500,000 or $250,000 depending on the type of building.

In low hazard areas (C, X) they will provide primary coverage with a deductible such as $50,000 or $100,000.

In moderate hazard areas (B, shaded X) insurers will do one or the other of these approaches depending on their risk appetite.

Given that setup, here is the insurance problem: The coverage provided by the insurer is subject to the zone remaining the same during the policy period. A fair approach would be for the insurance to remain in effect regardless of a zone change, subject to rerating or reevaluation at renewal, but that is not how the industry is operating (with possible exceptions of course).

In the example above, the policy covers properties in any zone except A or V. But the zone that applies is the one in effect “at the time of loss,” not the one in effect at the policy effective date! And, as mentioned, FEMA is in the process of, and will constantly be in the process of, revising flood zone designations to reflect changing flood exposures.

So, bottom line: The risk of a flood zone change rests with the insured, not the insurance company. The insurer gets to protect its own balance sheet, while the little old insured is left vulnerable!

What To Do About the Coverage Uncertainty

Property owners should know what zones their properties are in at the beginning of the policy year ---- and all during the policy year. There are companies who offer flood zone determinations – along with continuous zone change monitoring. In our work with clients we monitor the zone for a 30-year period via a third party service provider. If we find a zone change which triggers a coverage gap, we will have to take evasive action.

Beyond Insurance

Risk management is not just about insurance. It also involves the areas of loss prevention and loss mitigation. With respect to flood, these could include elevation of the property (most feasible with new construction), barriers, wet-proofing and more. Some resources can be accessed here:

https://www.fema.gov/media-library/assets/documents/6131

new construction

https://facilityexecutive.com/2016/01/question-of-the-week-have-you-addressed-flood-mitigation-strategies/

mitigation for commercial buildings

https://www.fema.gov/media-library-data/1443014398612-a4dfc0f86711bc72434b82c4b100a677/revFEMA_HMA_Grants_4pg_2015_508.pdf

mitigation when you cannot elevate

https://floodbreak.com/about/success-stories/fema-flood-mitigation-best-practices/

flood barriers

https://science2017.globalchange.gov/chapter/executive-summary/

increasing rainfall

Frank Licata is the president of Licata Risk & Insurance Advisors, Inc., Boston.

Tags:

Spotlight Content

MORE FROM Spotlight Content

NEREJ's 2026 Industrial Review Spotlight

The New England Real Estate Journal is pleased to present Industrial Review 2026, a special publication highlighting the people, projects and properties shaping New England’s industrial real estate market.

Quick Hits

Columns and Thought Leadership

Shallow-bay wins on 495/128: A renewal-driven market with a thin pipeline - by Nate Nickerson

The Boston industrial market entered mid-2025 in a bifurcated state. Large-block vacancy remains elevated, while shallow-bay along the 495/128 corridor continues to prove resilient. Fieldstone’s focus on this geography positions us squarely in the middle of a renewal-driven, supply-constrained

As legacy names recalibrate, new entrants are moving in with fresh capital, new technologies, and business models tailored to today’s supply-chain needs - by Michael Harrington

Southern New Hampshire’s industrial market has always punched above its weight. For decades, the region has attracted a mix of advanced manufacturing, beverage and food producers, logistics operators, and specialty

Limited supply fuels landlord‑friendly conditions in Rhode Island’s industrial market - by Julie Freshman and George Paskalis

As we enter the spring of 2026, the Rhode Island industrial real estate market stands on stable footing, following several years of resilience fueled by constrained supply, steady demand, and dynamic economic conditions.

How do we manage our businesses in a climate of uncertainty? - by David O'Sullivan

These are uncertain times for the home building industry. We have the threat of tariffs mixed with high interest rates and lenders nervous about the market. Every professional, whether builder, broker, or architect, asks themselves, how do we manage our business in today’s climate? We all strive not just to succeed, but