(1).png)

News:

Owners Developers & Managers

Posted: July 29, 2016

2016 mid-year office market update: Greater Portland remains safe investment - by Matt Barney

Matthew Barney, Malone Commercial Brokers

Matthew Barney, Malone Commercial BrokersThe first half of 2016 continued the positive trend for Greater Portland, with landlords and sellers now realizing the benefits of a more favorable market.

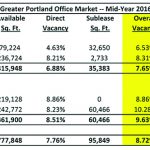

• Vacancy/absorption remained unchanged on the whole, but the downtown market tightened by nearly 1% while the suburbs increased in vacancy by 1.3%.

• Leasing activity increased by 23% over the first six months of 2015, with large-tenant leasing and renewals (10,000+ s/f) nearly double the normal average.

• Large, “For Lease” floorplate options remain scarce downtown, but the suburbs now offer a half-dozen or so 10,000+ s/f spaces for tenants needing an alternative.

• Office sale activity slowed in the first six months, but demand remains at an all-time high in Greater Portland from local, regional and national investors.

Overall vacancy (both direct and sublease) came in at 8.72% as of mid-year, but with contrasting results by submarket. Downtown posted vacancy of 7.65%, the lowest since 2006, with the Class A sector now at 6.53% (a 2008 level). In contrast, the suburban market increased in vacancy to 9.63%, due mostly to an increase in available sublease space (on a direct basis, the suburban market was even with year-end 2015 at 7.76%).

Overall vacancy (both direct and sublease) came in at 8.72% as of mid-year, but with contrasting results by submarket. Downtown posted vacancy of 7.65%, the lowest since 2006, with the Class A sector now at 6.53% (a 2008 level). In contrast, the suburban market increased in vacancy to 9.63%, due mostly to an increase in available sublease space (on a direct basis, the suburban market was even with year-end 2015 at 7.76%).

Large-Tenant leases remained active in the first half, with notable renewals by Wells Fargo (12,899 s/f) and Prudential (51,831 s/f) at Two Portland Sq., and WEX (42,000 s/f) at 95-97 Darling Ave., along with new leases by The Beacon Group (17,581 s/f) at 280 Fore St. and Sebago Technics (18,435 s/f) at 75 John Roberts Rd.

For tenants needing contiguous space of 10,000 s/f or more, the options downtown remain limited – 14,000 s/f and 12,671 s/f spaces are available at 100 Middle St. and One Monument Sq. (respectively), with a new 5-story, 48,000 s/f building poised to break ground this year at 16 Middle St. In contrast, the suburban market now “has the goods”, with multiple options in South Portland and Westbrook for tenants seeking contiguous space from 13,000 s/f up to 135,000 s/f.

Going forward: • Downtown, Class A rents will increase as supply outpaces demand. While the historic, average annual increase is only 1.8%, asking rents are already up 5% - 10% for tower spaces. It’s inevitable that renewals and new lease pricing will bump. New construction must be on the horizon for 2017.

The suburban market should see a jump in leasing activity, simply by having available, large-floorplate options and free parking. Downtown parking now ranges between $140 to $150/space/month for desired locations, which equates to a net-rent-equivalent of $7.00 - $9.00/SF. Whether company or employee paid, this is now a noticeable burden.

Landlords should still be cautious in this favorable market, continuing to focus on tenant retention rather than a drastic increase in pricing. Tenants, on the other hand, should have broker representation now more than ever. Both parties want the same outcome and good brokers can effectively guide both sides to that outcome.

Matthew Barney is a broker with Malone Commercial Brokers, Portland, ME.

MORE FROM Owners Developers & Managers

The Westin Portland Harborview to host exclusive VIP pop-up with The Woods Maine July 24–26

Portland, ME The Westin Portland Harborview will introduce an exclusive, limited-time pop-up shop with The Woods Maine, taking place July 24–26 in the city’s Arts District. This elevated retail experience brings The Woods Maine, the acclaimed Maine lifestyle brand behind the popular retail shop in Norway, Maine, directly to hotel guests and the local community.

Quick Hits

(1).png)

Columns and Thought Leadership

Retail infill strategy to activate Pawtucket’s Conant Thread District - by Gaetan Kashala

Until recently, the Conant Thread District consisted of approximately 150 acres of underutilized industrial land spanning Pawtucket and Central Falls. Today, the area is one of the most significant

Florida ruling raises bar for condo terminations and buyouts - by Michael Karsch

On October 14, 2025, in a landmark decision with significant implications for the Florida real estate market, the Supreme Court of Florida formally denied Two Roads Development’s (TRD Biscayne LLC) petition for review in its long-running case against unit owners of Biscayne 21,

IREM president’s message: Our new reality - Staying ahead of supply chain delays - by Yoany Vargas

Supply chain delays are slowing construction, ratcheting up operating costs, and extending turnover timelines across Greater Boston, directly reducing revenue and increasing the workload for multifamily and

Revitalized Town Centers: Retail??? - by Carol Todreas

It is now widely accepted that customers want to shop in person at physical stores. Brands know that they do better business in a physical store than just on line so they want to open stores. Demand for retail space by digital merchants, local entrepreneurs, and newly developed national chains