(1).png)

News:

Owners Developers & Managers

Posted: May 27, 2016

Boston’s top city rating in real estate will continue to carry markets into third decade of 21st century - by Web Collins

Webster Collins, CBRE/New England

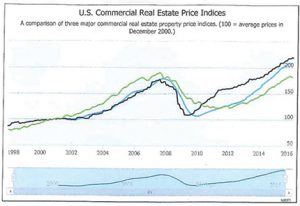

Webster Collins, CBRE/New EnglandIt has been a long climb back since the Great Recession. We spent two years on the downside when the market fell out of bed—December 2007 through 2009—and it took 3.5 years to recover on the upside. We have had three very good years since as illustrated in the graph below:

The market has now peaked in Boston. This article will address three market observations and conclude as to the likely patterns ahead.

Signals of a Market Peak If one studies the actions of Boston properties, the last thing you will see is the start of construction in Boston’s urban core without a lead tenant. That said, three major players have announced ground up construction on speculatively built new office buildings to total ±1 million s/f.

At the time of their announcement, Q1 2016 market statistics suggest 883,000 s/f of negative absorption for the market as a whole. It is a sure sign of market peaking when speculative construction takes place. This is evident in the apartment market with Class A product. 2015 saw 6,767 units of new construction; that market is now taking a breather with a 33% pullback in new construction projected for 2016.

Price Change When markets peak, changes in pricing typically occur. National statistics published by Moody’s, Real Capital Analytics and Green Street Advisors show mixed trends from a -1.1% decline Q1 2016 to as little as -0.5% decline for Q1 2016.

Price change is primarily attributed to changes in interest rates from the Federal Reserve’s rate adjustments from last fall. Real estate pricing is clearly impacted by the volatility being experienced in the capital markets.

What brought this into my mind is my recent email exchange with Fantini & Gorga on financing spreads. There is a lot of confusion ‘when trying to compare pricing across industry lenders.’ Just because markets are at their peak and prices change, this does not mean that Great Recession signs are again on the horizon. They are not.

What brought this into my mind is my recent email exchange with Fantini & Gorga on financing spreads. There is a lot of confusion ‘when trying to compare pricing across industry lenders.’ Just because markets are at their peak and prices change, this does not mean that Great Recession signs are again on the horizon. They are not.

On May 12, 2016, I attended a program where CBRE’s chief economist, Jeff Havsy was a featured speaker. His views are that we may see a mild pullback in 2018, as a result of a slowdown in job growth due skill/personnel mismatch, a strong dollar, and an environment with raising interest rates. At most, we are looking at three quarters of job loss and two quarters of negative GDP.

Basel III Rules Likely to Affect Commercial Real Estate This is the title of a recent ULI publication. It is banks ‘risk-weighting’ for what are called “high-volatility commercial real estate loans.” Under new regulations, LTV ratios must be 80% or less, but more importantly, actual cash of at least 15% must be contributed before bank funding can take place. The required equity is based on actual cost rather than as-completed value.

Banks are the traditional source for construction loans. Construction loans from banks clearly will be harder to come by, which will take off the froth that existed in the market in 2015.

Conclusion Boston continues to be a magnet for acquisition of prime properties. That said, CBRE suggests a two-quarter mild recession in the 2018 timeframe. While adjustments in market pricing are expected to take place and the economies of new construction may shrink, I believe that Boston’s top city rating in the world of real estate will continue to carry our markets into the third decade of the 21st century.

Webster Collins, MAI, CRE, FRICS is an executive vice president and partner within CBRE’s Valuation and Advisory Group, Boston.

MORE FROM Owners Developers & Managers

The Westin Portland Harborview to host exclusive VIP pop-up with The Woods Maine July 24–26

Portland, ME The Westin Portland Harborview will introduce an exclusive, limited-time pop-up shop with The Woods Maine, taking place July 24–26 in the city’s Arts District. This elevated retail experience brings The Woods Maine, the acclaimed Maine lifestyle brand behind the popular retail shop in Norway, Maine, directly to hotel guests and the local community.

Quick Hits

Columns and Thought Leadership

Revitalized Town Centers: Retail??? - by Carol Todreas

It is now widely accepted that customers want to shop in person at physical stores. Brands know that they do better business in a physical store than just on line so they want to open stores. Demand for retail space by digital merchants, local entrepreneurs, and newly developed national chains

IREM president’s message: Our new reality - Staying ahead of supply chain delays - by Yoany Vargas

Supply chain delays are slowing construction, ratcheting up operating costs, and extending turnover timelines across Greater Boston, directly reducing revenue and increasing the workload for multifamily and

Retail infill strategy to activate Pawtucket’s Conant Thread District - by Gaetan Kashala

Until recently, the Conant Thread District consisted of approximately 150 acres of underutilized industrial land spanning Pawtucket and Central Falls. Today, the area is one of the most significant

Florida ruling raises bar for condo terminations and buyouts - by Michael Karsch

On October 14, 2025, in a landmark decision with significant implications for the Florida real estate market, the Supreme Court of Florida formally denied Two Roads Development’s (TRD Biscayne LLC) petition for review in its long-running case against unit owners of Biscayne 21,