(1).png)

News:

Owners Developers & Managers

Posted: June 12, 2026

Connecticut student housing: A niche sector comes of age - by Anastasia Friedman

National Context: Niche commercial real estate sectors – medical office, net lease, self-storage, and student housing – are moving from the fringe to the core of institutional portfolios. As traditional office markets post diminished value expectations and soft tenant retention, the niche category is moving in the opposite direction, drawing capital that seeks defensive income and predictable cash flow. The PwC Investor Survey places the niche sectors’ average forecast value change over the next twelve months at 1.4%, against negative 2.3% for the eighteen office markets surveyed.

For student housing specifically, the PwC Investor Survey first-quarter 2026 figures describe a sector still attracting capital even as its fundamentals normalize. The national overall capitalization rate averaged 5.84%, down ten basis points from the prior quarter and twenty from a year earlier, while the unleveraged discount rate averaged 8.38%. Forecast value change over the next twelve months averaged 2.6%, and marketing time averaged 2.7 months. The cautionary signal sits in the income line: year-one market rent change averaged 3.75%, down sixty-seven basis points year over year, even as the expense-change average rose to 3.61%. Compressing cap rates and rising values coexist with decelerating rent growth and climbing costs.

The national outlook attributes much of that rent deceleration to supply outpacing enrollment in saturated university markets – a risk sharpened by demographics. The number of United States high-school graduates is projected to decline beginning in 2026, potentially by as much as thirteen% by 2041, with the Northeast among the regions expected to contract. Connecticut sits squarely in that declining region, which makes its university markets a useful local test of the national thesis: where does new supply still find demand, and where does it not?

Sources: PwC Investor Survey, 1Q 2026 (National Student Housing Market); PwC and Urban Land Institute, Emerging Trends in Real Estate 2026.

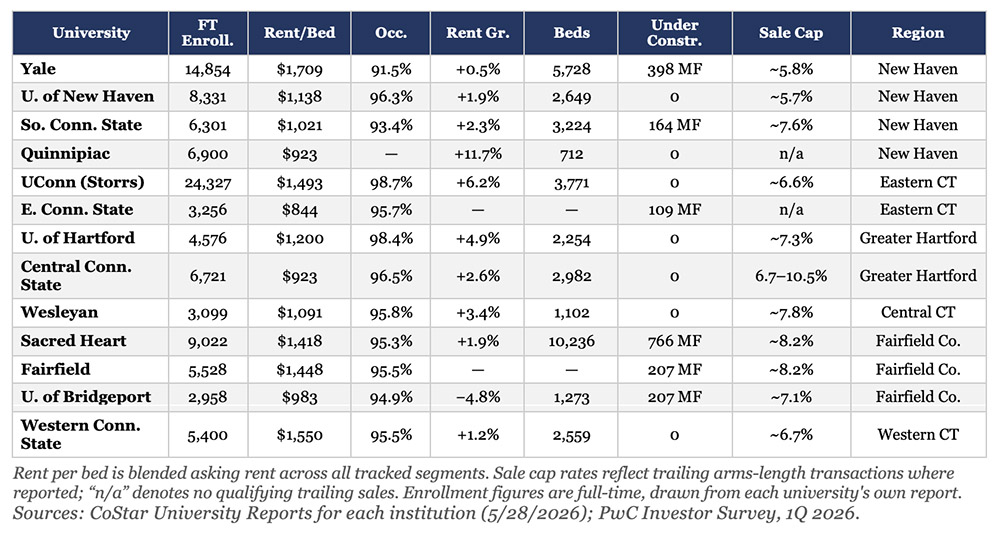

The Connecticut Survey at a Glance: Thirteen Connecticut university markets, surveyed as of May 2026, span the full national range on every measure that matters – from a 5.8% institutional cap rate in New Haven to older Bridgeport stock above 8%, and from a 6.2% rent gain at Storrs to a 4.8% decline in Bridgeport (see Chart 1).

University Market Profiles

Yale University – New Haven: Yale anchors the New Haven region and the entire survey on pricing. The university enrolls 14,854 full-time students, weighted toward graduate study (8,049 graduate against 6,805 undergraduate), with dormitory capacity near 5,600 leaving roughly 9,278 students seeking off-campus housing. The tracked off-campus market spans 111 properties and 5,728 beds at a blended asking rent of $1,709 per bed, the highest in the set, against 91.5% occupancy, the lowest. A small purpose-built student segment of eight properties and 237 beds average a 1911 vintage and $1,244 per bed, with student rents off 3.7% over the year, while multifamily product within a ten-minute walk command $1,741 per bed.

Yale produced the deepest transaction record of any market studied: ten arms-length sales over the trailing year averaging $270,300 per unit at a 5.8% average capitalization rate, ranging from 5.3% to 6.5%. The benchmark trade was The Haven on College, a 160-unit, 2015-vintage asset that sold for $57.5 million ($359,375 per unit). New supply remains active, with 405 multifamily beds delivered over the past four quarters and 398 under construction, including ConnCAT Place on Dixwell and Estelle New Haven.

Sources: CoStar University Report, Yale University (5/28/2026); PwC Investor Survey, 1Q 2026.

University of New Haven – West Haven: University of New Haven presents the clearest demand-side growth story in the survey. Full-time enrollment reached 8,331, up a striking 10.5% over the year and led by graduate expansion, while dormitory capacity held roughly flat – pushing the non-dorm population to about 5,531. The off-campus market tracks 52 properties and 2,649 beds at a blended $1,138 per bed and 96.3% occupancy, with rent growth of 1.9%. A modest student segment of three properties and 177 beds overlap the New Haven core shared with Yale and Southern Connecticut State.

Investment evidence is institutional in character: four trailing sales averaging $220,000 per unit at a 5.7% average capitalization rate – the lowest in the survey alongside Yale – anchored by genuinely New Haven-grade product. The market recorded 191 multifamily beds delivered over the past four quarters and no purpose-built student pipeline, leaving demand growth to be absorbed by existing and multifamily stock.

Sources: CoStar University Report, University of New Haven (5/28/2026); PwC Investor Survey, 1Q 2026.

Southern Connecticut State University – New Haven: Southern Connecticut State joins Yale and New Haven within the New Haven region. The public institution enrolls 6,301 full-time students against dormitory capacity near 2,300, leaving roughly 4,010 students off campus. The tracked market comprises 66 properties and 3,224 beds at a blended $1,021 per bed, 93.4% occupancy, and 2.3% rent growth. Unlike most regional publics in the survey, Southern carries a measurable purpose-built student segment of nine properties and 310 beds at an average 1925 vintage, with student rents averaging $971 per bed.

Four trailing sales averaged $187,800 per unit at a 7.6% average capitalization rate and 6.2% average vacancy at sale, reflecting older New Haven stock. Modest supply is active, with 164 multifamily beds under construction at 500 Blake St. and 122 delivered over the past four quarters at 340 Dixwell.

Sources: CoStar University Report, Southern Connecticut State University (5/28/2026); PwC Investor Survey, 1Q 2026.

Quinnipiac University – Hamden: Quinnipiac posts the strongest headline rent growth in the survey, though on a thin base that warrants caution. Full-time enrollment is 6,900 against a large dormitory base near 4,700. The off-campus market tracks just seven properties and 712 beds, but blended rent growth registered 11.7% over the year, with both the sub-ten-minute and beyond-twenty-minute rings running near 11%. There were no deliveries, no beds under construction, and no qualifying sales in the trailing year.

The absence of transaction support and the small tracked inventory suggest the rent-growth figure reflects a small-sample effect rather than a broad market move, and it should be read alongside the deeper New Haven evidence rather than in isolation.

Sources: CoStar University Report, Quinnipiac University (5/28/2026); PwC Investor Survey, 1Q 2026.

University of Connecticut – Storrs (Eastern CT): The University of Connecticut is the only true student-housing-driven market in the survey and the largest by enrollment, with 24,327 full-time students against dormitory capacity near 12,000. Off-campus product tracks 15 properties and 3,771 beds at a blended $1,493 per bed, 98.7% occupancy – the highest in the set – and 6.2% rent growth, also the strongest. Purpose-built student housing dominates the segment: seven properties and 1,918 beds at 98.1% pre-leasing and a 1971 average vintage.

The defining event was supply. Student inventory jumped 86.8% in a single year as The Standard at Four Corners delivered 891 beds (Landmark Properties, 2025), yet occupancy and rent growth held at the top of the survey – demand outran a substantial new delivery. Transaction evidence is thin, limited to one trailing sale (Eagle Court Apartments, $3.02 million, $335,333 per unit), with the market-trend capitalization rate near 6.6%.

Sources: CoStar University Report, University of Connecticut (5/28/2026); PwC Investor Survey, 1Q 2026.

Eastern Connecticut State University – Willimantic (Eastern CT)

Eastern Connecticut State rounds out the Eastern region. The public institution enrolls roughly 3,256 full-time students and carries one purpose-built student property, Meadowbrook Gardens (350 beds, 2017), priced near $638 per bed. The broader tracked market sits near $844 per bed at 95.7% occupancy. Notably, student occupancy and pre-leasing run softer than the surrounding multifamily – an 84% pre-lease against multifamily near 98% – the clearest student-versus-multifamily divergence in the survey.

A modest pipeline is active: 109 multifamily beds under construction at the Residences on Main (804 Main Street), making Eastern one of the few smaller markets with a live delivery. Sales evidence is limited and does not support a reliable capitalization-rate conclusion.

Sources: CoStar University Report, Eastern Connecticut State University (5/28/2026); PwC Investor Survey, 1Q 2026.

University of Hartford – West Hartford (Greater Hartford)

University of Hartford headlines the Greater Hartford region. Full-time enrollment is 4,576, up 3.9% over the year but still modestly negative on a five-year average – a recovery off a trough rather than sustained growth. The tracked market spans 21 properties and 2,254 beds at a blended $1,200 per bed, 98.4% occupancy, and 4.9% rent growth. Both the occupancy and rent-growth figures warrant a footnote: a single 785-bed property reports full occupancy, and the lone student property shows a data-revision rent spike, so the multifamily series is the more reliable signal.

Two trailing sales averaged $113,800 per unit at a 7.3% average capitalization rate (6.2% to 8.4%), classic older Hartford stock from 1900 to 1926. There were no beds under construction and 122 multifamily beds delivered over the past four quarters.

Sources: CoStar University Report, University of Hartford (5/28/2026); PwC Investor Survey, 1Q 2026.

Central Connecticut State University – New Britain (Greater Hartford)

Central Connecticut State is an entirely multifamily off-campus market with no purpose-built student inventory. The public institution enrolls roughly 6,721 full-time students against dormitory capacity near 2,400. The tracked market spans 80 properties and 2,982 beds at a blended $923 per bed, 96.5% occupancy, and 2.6% rent growth. Like most regional publics in the survey, Central faces enrollment headwinds, with a five-year average decline that acts as a structural counterweight to rent growth.

Eight trailing sales averaged $87,500 per unit, the lowest per-unit pricing in the survey, at capitalization rates spanning 6.7% to 10.5% – the standard older New Britain multifamily profile from the 1900-to-1925 vintage. No deliveries occurred over the past four quarters, and none are under construction.

Sources: CoStar University Report, Central Connecticut State University (5/28/2026); PwC Investor Survey, 1Q 2026.

Wesleyan University – Middletown (Central CT)

Wesleyan stands apart as an elite private in its own Central Connecticut submarket, with no purpose-built student inventory and an off-campus market that is entirely multifamily. Full-time enrollment is 3,099, essentially flat (down 1.0% over the year but slightly positive on a five-year average), against dormitory capacity near 3,000 that captures most demand. The tracked market spans 42 properties and 1,102 beds at a blended $1,091 per bed, 95.8% occupancy, and 3.4% rent growth. The walk-time gradient is steep: $1,267 per bed within a ten-minute walk of campus along Main Street, against $875 and $838 in the outer rings.

Five trailing sales averaged $125,800 per unit, all small older Middletown stock (1790 to 1985 vintage) within roughly a third of a mile of campus; no capitalization rates were reported on the trailing comps, with the market-trend rate near 7.8%.

Sources: CoStar University Report, Wesleyan University (5/28/2026); PwC Investor Survey, 1Q 2026.

Sacred Heart University – Fairfield (Fairfield County)

Sacred Heart leads the Fairfield County region on growth and supply. The private institution enrolls 9,022 full-time students, up 4.0% over the year and 7.4% on a five-year average – among the strongest demand profiles in the survey – against dormitory capacity near 3,600. The off-campus market is the largest tracked in the survey at 233 properties and 10,236 beds, blended $1,418 per bed, 95.3% occupancy, and 1.9% rent growth, with nearly all inventory situated beyond a twenty-minute drive in the Bridgeport multifamily market.

The development pipeline is the largest in the survey: 766 multifamily beds under construction – led by The August at Steelpointe Harbor (559 beds) – with 315 beds delivered over the past four quarters. Four trailing sales averaged $123,800 per unit at an 8.2% average capitalization rate (6.9% to 9.5%), reflecting older Bridgeport stock; the broader market-trend rate, informed by heavier institutional volume in prior years, sits nearer 6.7%.

Sources: CoStar University Report, Sacred Heart University (5/28/2026); PwC Investor Survey, 1Q 2026.

Fairfield University – Fairfield (Fairfield County)

Fairfield University is a selective private whose off-campus inventory, like Sacred Heart’s, clusters in the Bridgeport-adjacent multifamily market. Full-time enrollment is roughly 5,528 with strong demand fundamentals – high tuition, a large out-of-state share, and positive enrollment growth. Blended asking rent is $1,448 per bed at 95.5% occupancy. A thin but premium ten-to-twenty-minute ring posts the highest single-ring figure in the survey, reflecting a small, well-located inventory.

Fairfield shows a genuine supply response, with 207 multifamily beds under construction (455 Fairfield Avenue and 430 John Street). Three trailing sales averaged $144,200 per unit at an 8.2% average capitalization rate, with the comps clustering in Bridgeport.

Sources: CoStar University Report, Fairfield University (5/28/2026); PwC Investor Survey, 1Q 2026.

University of Bridgeport – Bridgeport (Fairfield County)

University of Bridgeport completes the Fairfield County region and registers the survey’s only negative rent trend. The private institution enrolls 2,958 full-time students against dormitory capacity near 830. The off-campus market tracks 33 properties and 1,273 beds at a blended $983 per bed and 94.9% occupancy, but rent growth was negative 4.8% over the year – the weakest in the survey. The market is entirely multifamily, with no purpose-built student inventory.

A pipeline of 207 multifamily beds is under construction (455 Fairfield Avenue and 430 John Street), and the market-trend capitalization rate sits near 7.1%. No qualifying arms-length sales closed in the trailing year.

Sources: CoStar University Report, University of Bridgeport (5/28/2026); PwC Investor Survey, 1Q 2026.

Western Connecticut State University – Danbury (Western CT)

Western Connecticut State anchors its own Western Connecticut submarket and posts the survey’s highest blended rent among the regional publics. The public institution enrolls roughly 5,400 full-time students. The tracked market spans 2,559 beds at a blended $1,550 per bed, 95.5% occupancy, and 1.2% rent growth. Unusually, rent rises with distance from campus, reflecting newer, larger product on the Danbury periphery rather than walk-to-campus stock.

Western carries the survey’s cautionary demand profile: full-time enrollment fell 5.2% over the year and 6.0% on a five-year average, with retention near 70% – the demographic pressure the national outlook flags for the Northeast. Two trailing sales averaged a 6.7% capitalization rate, anchored by the Ridgeway Place trade at $54.25 million ($282,552 per unit).

Sources: CoStar University Report, Western Connecticut State University (5/28/2026); PwC Investor Survey, 1Q 2026.

Connecticut Against the National Benchmark

Read as one market, the thirteen Connecticut universities both confirm and complicate the national picture. The survey’s blended rents run from $844 per bed at Eastern Connecticut State to $1,709 at Yale, and trailing sale capitalization rates bracket the national 5.84% average on both sides: New Haven’s institutional product at roughly 5.7% to 5.8% sits at or through the national mark, while older Bridgeport and New Britain stock carries an 8% or higher risk premium. Connecticut does not match the national average so much as define its range.

The national caution – that new supply is outpacing enrollment and dragging on rent growth – holds unevenly here, and the exceptions are the most instructive cases. The University of Connecticut absorbed an 86.8% one-year jump in student inventory, the 891-bed Standard at Four Corners, yet still posted the survey’s highest occupancy at 98.7% and strongest rent growth at 6.2%. Demand outran a very large delivery. University of New Haven shows the same logic from the demand side: a 10.5% enrollment surge against flat dormitory capacity, absorbed at 96.3% occupancy with institutional 5.7% cap-rate pricing. These are the markets where the niche sector earns its premium.

Where supply meets soft demand, the warning bites. University of Bridgeport posted the survey’s only negative rent trend, down 4.8%, even as 207 beds remain under construction. Western Connecticut State pairs the highest regional-public rent, $1,550 per bed, with a 5.2% enrollment decline and roughly 70% retention – the Northeast demographic pressure the national outlook flags, made local. Sacred Heart and Fairfield carry the survey’s heaviest pipelines, 766 and 207 multifamily beds, into a Bridgeport market that is already largely built out; whether that inventory leases at expected rents will turn on enrollment that the regional demographics do not obviously support.

The rent-growth spread tells the same story numerically. Against the national 3.75% year-one average, the Connecticut set runs from negative 4.8% at Bridgeport and 0.5% at Yale at the low end to 6.2% at Storrs and a thin-sample 11.7% at Quinnipiac at the high. The dispersion, not the average, is the point: in a contracting demographic region, student-housing performance is becoming a market-by-market question of whether a given campus still draws students faster than developers can add beds.

Sources: CoStar University Reports for each institution (5/28/2026); PwC Investor Survey, 1Q 2026; PwC and Urban Land Institute, Emerging Trends in Real Estate 2026.

Outlook

The national thesis is sound: student housing has earned its place as a core niche holding, and Connecticut’s strongest campuses – Storrs, New Haven – trade and perform accordingly. But the same demographic cliff that makes the sector defensive nationally makes it selective regionally. Over the next several years, the Connecticut markets most exposed are those layering new supply onto flat or declining enrollment, particularly in Fairfield County and at the demographically pressured regional publics. The markets best positioned are those with demonstrated demand depth and institutional-grade product, where occupancy has already absorbed substantial new beds. For investors and appraisers alike, the discipline the data demands is the same one the national survey implies: underwrite the campus, not the sector.

Sources: CoStar University Reports for each institution (5/28/2026); PwC Investor Survey, 1Q 2026 (National Student Housing Market); PwC and Urban Land Institute, Emerging Trends in Real Estate 2026.

Anastasia Friedman, MAI is a commercial real estate appraiser in Connecticut and the New York Metropolitan Area.

MORE FROM Owners Developers & Managers

Two Pence Market opens in Milton Village - developed by the team behind local restaurant Steel & Rye

Milton, MA After months of anticipation, Two Pence Market welcomed its first guests on Wednesday, July 29, introducing a vibrant new neighborhood destination for fresh food, specialty

Quick Hits

(1).png)

Columns and Thought Leadership

Revitalized Town Centers: Retail??? - by Carol Todreas

It is now widely accepted that customers want to shop in person at physical stores. Brands know that they do better business in a physical store than just on line so they want to open stores. Demand for retail space by digital merchants, local entrepreneurs, and newly developed national chains

IREM president’s message: Our new reality - Staying ahead of supply chain delays - by Yoany Vargas

Supply chain delays are slowing construction, ratcheting up operating costs, and extending turnover timelines across Greater Boston, directly reducing revenue and increasing the workload for multifamily and

Retail infill strategy to activate Pawtucket’s Conant Thread District - by Gaetan Kashala

Until recently, the Conant Thread District consisted of approximately 150 acres of underutilized industrial land spanning Pawtucket and Central Falls. Today, the area is one of the most significant

The legislature has spoken: New Hampshire doubles down on housing in commercial zones - by John Sokul

Last year, the New Hampshire Legislature enacted HB 631, a landmark housing measure requiring municipalities to permit multifamily housing in commercially zoned districts. The law generated