(1).gif)

News:

Finance

Posted: August 12, 2022

CT real estate taxes – What? Really!? Why?

“A tax is a fine for doing well, a fine is a tax for doing wrong.” - Mark Twain.

Mr. Clemens is a Connecticut treasure. The man owns great quotes that sound whimsically profound either spoken or thought out loud. He was also a lousy businessman and prone to aggrievement.

This isn’t another article complaining of high taxes in CT. They are quite high, fourth in the nation behind New Jersey, Illinois, and New Hampshire. That’s clearly the fault of liberals who want to spend too much, conservatives that don’t want to govern, and our fellow citizens who can’t be bothered to either pay attention or vote. It’s also not because of those things at all.

No, my grievance is with how and when real estate taxes are calculated and due in Connecticut. It’s bizarre and confusing for property owners, which leads to many a needless time-wasting conversation for our assessors. They explain and explain, again and again, patiently mostly, day after day, morning and afternoon, all day, every day, to the young and to the old, and to the middle-aged and to the very old, so often to the very old, like Sisyphus doomed to push boulders of unheard words up eternal hills, they explain as best they can. But why is it like this? They struggle to answer. Why are Connecticut real estate taxes so confusing?

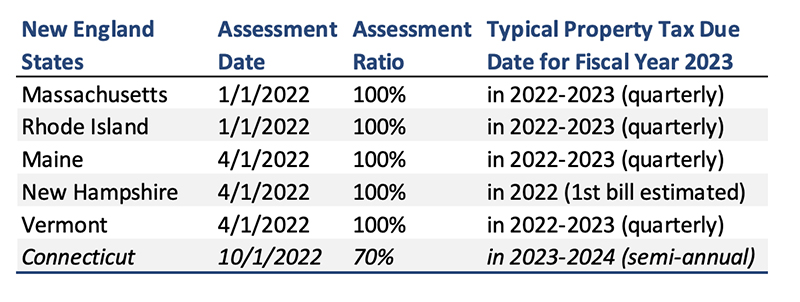

• Why are tax payments based on a Fiscal Year value date two calendar years prior to the bill being due? (No other New England state does this.)

• Why do we apply a 70% assessment ratio when all other New England states plus New York & New Jersey use 100%?

• Are they trying to trick us into thinking we’re getting some kind of deal by not paying taxes on the 100% assessment? (We’d pay the same tax amount with higher assessed values, as mill/tax rates would be lowered proportionally, because the tax rate is just the budget divided by the grand list total of all real estate values.)

• Do they take us for fools!?

• And who are they and why are they after us?

As with many things Connecticut, it started long ago… Our research suggests the earliest known tax records are 8,000 years old and were maintained on clay tablets. In the 11th century, Lady Godiva rode naked on a horse in England to protest her husband’s property tax assessment. He received an abatement. Not exactly pertinent, either the mention of clay tablets or this naked anecdote, but the latter is fun food for thought if you plan to appeal your taxes.

After the pilgrims landed in Plymouth, their original pact created taxes and assessments. Before we had a monetary system, taxes were paid as a percentage of crops grown. In the 1700-1800s, farmers took turns being the assessor. But they had to harvest their fields before starting assessment work. That’s why Connecticut uses October 1st as the date of value. All surrounding states and New Jersey use either January 1st or April 1st. Didn’t they also have crops, you may be asking yourself?

Why do CT towns use a 70% ratio?

CT General Statute 12-62a(b): Each such municipality shall assess all property for purposes of the local property tax at a uniform rate of seventy per cent of present true and actual value.

In 1798, the United States was facing a potential war with France and needed funds to strengthen the military. Congress enacted a $2 million direct tax on all 16 states. The tax was known as the ‘window tax’ because assessors were instructed to estimate values based on the number and size of windows and doors. This was not appreciated, and many assessors were beaten by small bands of property owners.

During the Great Depression in the 1930s, towns began assessing property at less than fair market value to 1) ease tax burdens and 2) because properties began selling for less. This ended in the 1960s when states raised assessed values to “market.”

After the Great Depression, most Connecticut towns began using assessment ratios of 60% to 65%. In 1972, the Governor’s Commission on Tax Reform suggested all municipalities assess property at 100% of fair market value and doing away with fractional assessments “because they made it harder for taxpayers to spot increases in assessed values”. Instead, in 1974’s Public Act (PA) 74-299 the Connecticut legislature required all municipalities to assess property at 70% of fair market value. (Prior to this, towns had different assessment dates and ratios. So, some progress was made but not to the extent recommended by the Governor’s Commission. Because they take us for fools.)

Why are CT tax payment due dates unique from surrounding states?

CT General Statute 12-142: Installments: due date: This law provides municipalities the ability to determine if tax bills are due in a single installment, two semi-annual payments or four quarterly payments…subject to the provisions of section 7-383.

Section 7-383 Due date of tax levy: This law requires the first tax levy payment to be collected on the “first day of such fiscal year”….“beginning the first day of July”.

CT General Statute 12-80c(b): “Notwithstanding the provisions of section 7-383” .… This law requires the tax collector to send a tax bill prior to July 1 in an amount equal to 50% of the tax burden.

In Connecticut, a property owner pays property taxes based on an October 1, 2021 grand list date, with payments due in July 2022 and January 2023. Only Connecticut and New Hampshire have semi-annual bills, although several communities opt for quarterly payments if state statues permit. New Hampshire estimates a property value in April, issues an estimated property tax bill in July and the final tax bill is in December. All valuations, taxes and calculations are dealt with in a single calendar year.

Most New England states have quarterly tax payments that generally correspond with the fiscal year, as shown on the following chart.

After perusing Chapters 203 and 204 of the CT statutes on Property Tax Assessment and Local Lev /Collection of Taxes (both are in section 12 if you are interested – you are not interested), there is no indication why we’ve chosen our two specific tax dates. Our research failed to unearth any explanation. One of life’s little mysteries.

Although Connecticut real estate taxes are universally seen as confusing, our legislature has no plan to change things for the better. Assessors and others tasked with explaining CT real estate taxes are therefore encouraged to refer all such future inquiries from citizens and internet trolls alike directly to our state legislature. I encourage this because I am aggrieved, and because I am also strangely pleased when strangers suffer until provoked to see things my way. Ask them to cast out the 70% assessment ratio and to call for payment due dates that correspond to the same fiscal year.

But let’s keep our October 1st valuation date. Because we’re different and, let’s be honest, we’re better.

Also, we need to move away from nutmeg. Its lame.

Connecticut – the better state!

It works both for our well-earned arrogance and to promote our tourism.

Anyway, if nothing changes for the better and it probably won’t, be kind to your assessor.

“In this world, nothing is certain but death and taxes.” Benjamin Franklin

Special Thanks to the following CT Assessors: Brian Penney (Hartford), Walter Topliff (Somers & Willington), Lawrence LaBarbera (Windsor), Thomas DeNoto (Bristol)

Josephine Aberle, MAI, is managing director at Valbridge Property Advisors, Hartford, Conn. - This was co-written by Patrick Craffey, MAI.

Referenced Sources:

A report on Connecticut Property Tax Administration and Exemptions, Theodore R. Smith 1970

History of Connecticut Assessors, Volumes 1-4: CAAO Research/Historian Committee

A Brief History of Property Tax, Richard Henry Carlson, September 1, 2004

A Discovery: 1798 Federal Direct Tax Records for Connecticut, Judith Green Watson, Spring 2007

Connecticut General Statutes

MORE FROM Finance

Washington Trust finances $28.8 million construction loan for 104-unit The Village at South County Commons

South Kingstown, RI The Washington Trust Company (Washington Trust) has financed a $28.8 million construction loan for new multifamily housing in Washington County.

(1).gif)

Quick Hits

Columns and Thought Leadership

Massachusetts real estate transfers over $1 million face new tax rules as of November 1st - by Daniel Meyer

Attention to owners of real estate in the Commonwealth (and the title companies and other professionals who advise them), the Massachusetts Department of Revenue (the “DOR”) recently adopted a new “millionaire’s tax” via 830 CMR 62B.2.4

Are appraisers on the same page as the assessor? - by Richard Seman

The purpose of this article is to address problematic or confusing issues which may help assessors and appraisers to better understand how to value real estate for tax assessment purposes.

Reverse exchanges and the challenges of a competitive real estate market - by Michele Fitzpatrick

Our current, highly competitive real estate market poses specific challenges for investors who are considering taking advantage of a tax-deferred 1031 exchange. In this market, investors will have no problem selling their current property if priced properly, but they may find it difficult to find a suitable replacement property

The focus on price per s/f compared to the comparable sales used in the appraisal report - by Dennis Chanski

Over the past several weeks, I have completed appraisal assignments for private clients. Interestingly, after submitting these appraisals, I received several phone calls – not to question the value, content, or any incorrect information, but rather to discuss the price per s/f compared to the comparable sales used in the report.