(1).png)

News:

Owners Developers & Managers

Posted: January 16, 2026

New England hotel development pipeline up year-over-year - by JP Ford

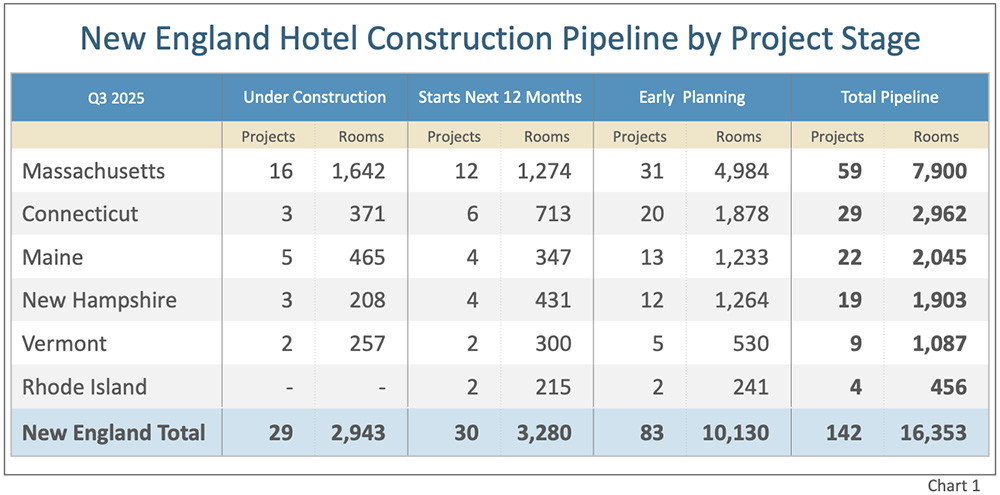

According to Lodging Econometrics’ (LE’s) U.S. Hotel Construction Pipeline Trend Report, the New England region’s pipeline reached 142 projects with 16,353 rooms at the end of Q3 2025. This marks a slight year-over-year (YOY) increase of 1% in projects and rooms from Q3 2024’s figures of 141 projects and 16,197 rooms. Massachusetts dominates the regional hotel construction landscape, claiming 59 projects totaling 7,900 rooms – representing 42% of all projects and 48% of rooms in the hotel pipeline in New England. Following Massachusetts, is Connecticut with 29 projects/2,962 rooms, then Maine with 22 projects/2,045 rooms. New Hampshire follows with 19 projects and 1,903 rooms, while Vermont has 9 projects comprising 1,087 rooms. Rhode Island rounds out the region with the smallest pipeline: 4 projects totaling 456 rooms. (See Chart 1)

New England’s hotel construction pipeline by project stage showed marginal change at the Q3 2025 close, with 29 projects and 2,943 rooms under construction. Looking ahead, 30 projects totaling 3,280 rooms are scheduled to begin construction anytime within the next 12 months, expanding 11% by projects and 16% by rooms YOY. New England hotel projects in the early planning stage remain unchanged, compared to the previous year, standing at 83 projects with 10,130 rooms. Early planning projects are those that are more than twelve months away from starting construction.

Massachusetts leads all stages of the New England construction pipeline with 16 projects/1,642 rooms under construction, 12 projects/1,274 rooms scheduled to start anytime within the next 12 months, and 31 projects/4,984 rooms in early planning.

Through the third quarter of 2025, in New England, 22 new hotels opened adding 2,237 rooms to the open & operating supply. LE analysts are forecasting a total of 27 projects/2,685 rooms to open across New England in 2025, for a 1.2% room supply growth rate. LE is forecasting another 17 projects/1,678rooms to open in 2026, and 18 new hotels with 1,881 rooms to open by year-end 2027.

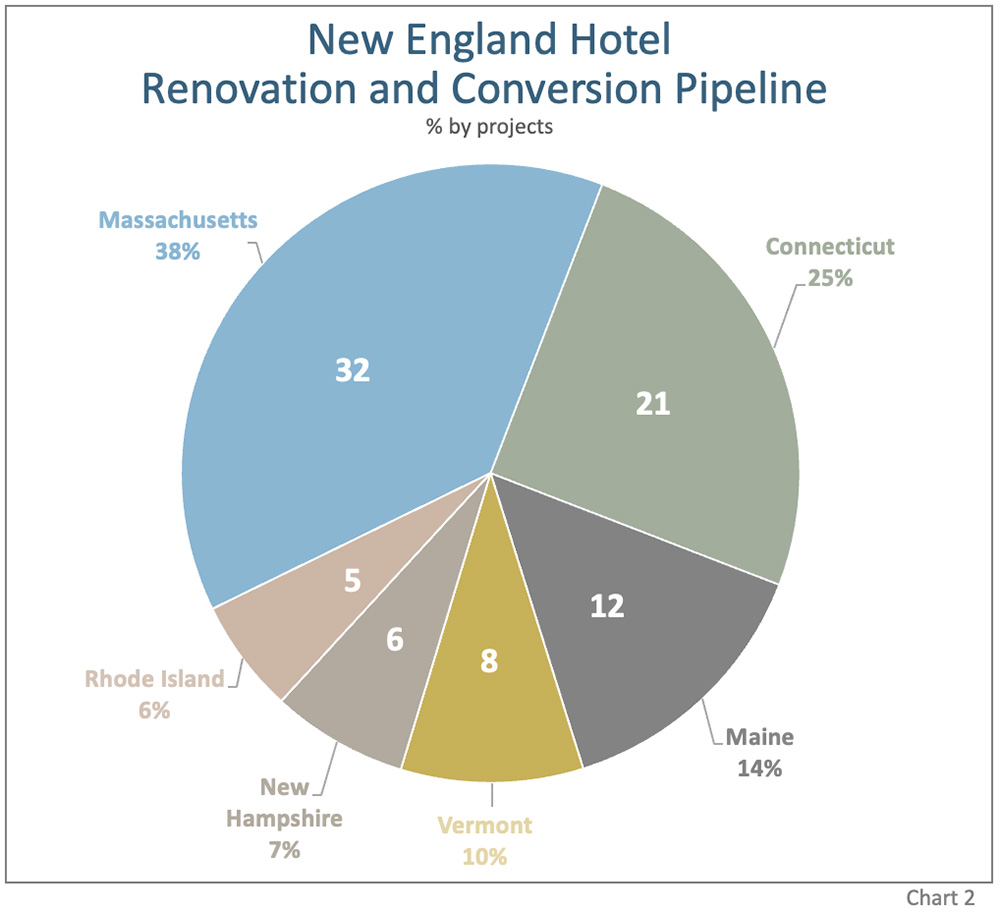

Hotel renovation and conversion activity across New England demonstrated moderate growth at the Q3 2025 close as well, with year-over-year increases of 12% in projects and 7% in rooms. The region has 84 properties encompassing 8,870 rooms undergoing either a renovation or brand conversion. Massachusetts leads these repositioning efforts with 32 projects and 4,500 rooms under renovation or conversion. Connecticut follows with 21 projects totaling 2,104 rooms, while Maine has 12 projects with 760 rooms. Vermont has 8 projects comprising 603 rooms, New Hampshire shows 6 projects with 418 rooms, and Rhode Island rounds out the region with 5 projects totaling 485 rooms. (See Chart 2)

At the end of Q3 2025, three major hospitality franchise companies dominate New England’s hotel pipeline, with Hilton Worldwide, Marriott International, and IHG Hotels & Resorts collectively representing 57% of all planned projects. Within these companies, the standout brands were Home2 Suites by Hilton, Residence Inn by Marriott, and Holiday Inn Express from IHG. However, a substantial portion of the region’s pipeline – 31% of all projects – presently consist of independent, unbranded projects. A high percentage of these currently unbranded projects will likely select a brand as they progress through the pipeline.

For more information on the hotel development pipeline or hotel transactions in New England, or any individual market in the U.S., global city, country, or region: contact Lodging Econometrics 603.431.8740, ext. 0025, or info@lodgingeconometrics.com.

Lodging Econometrics is the leading provider of global hotel development intelligence, decision maker contacts, and unparalleled customer service. With decades of lodging industry experience, a real-time pulse on market trends, and extensive knowledge of key decision makers, LE delivers actionable business development programs for hotel franchise companies looking to accelerate their brand growth, hotel ownership and management companies seeking to expand their portfolios, and lodging vendors/suppliers looking to increase their sales.

JP Ford, ISHC, senior vice president and director of global business development. Ford leads all the strategic sales initiatives globally for Lodging Econometrics. He is an industry leading trusted advisor to franchise companies looking to identify branding opportunities; ownership and management groups looking to add real estate assets and management contracts to their portfolios; lodging industry vendors seeking to increase product distribution and Wall Street Analysts interested in evaluating hotel development, hotel sales transaction trends, and assessing investment potential in hotel companies and markets.

Ford chairs the committee responsible for gathering nominations and selecting the finalists for the Americas Lodging Investment Summit (ALIS) “Development of the Year” awards, which recognizes the most outstanding achievement in hotel construction and design in the Americas. Ford is also a committee member of the Caribbean & Latin America Conference (CALA), which selects the “Development of the Year Award” in Latin America. Ford is a speaker at various hotel industry events and conferences and regularly contributes to several lodging real estate publications. He is a member of the International Society of Hospitality Consultants (ISHC).

MORE FROM Owners Developers & Managers

$3.8 million Housing Development Incentive Program award advances Greystarts Whittenton Mills modular housing development

Taunton, MA Greystar has received a $3.8 million Housing Development Incentive Program (HDIP) award from the Massachusetts Executive Office of Housing and Livable Communities to support the

(1).png)

Columns and Thought Leadership

Florida ruling raises bar for condo terminations and buyouts - by Michael Karsch

On October 14, 2025, in a landmark decision with significant implications for the Florida real estate market, the Supreme Court of Florida formally denied Two Roads Development’s (TRD Biscayne LLC) petition for review in its long-running case against unit owners of Biscayne 21,

Retail infill strategy to activate Pawtucket’s Conant Thread District - by Gaetan Kashala

Until recently, the Conant Thread District consisted of approximately 150 acres of underutilized industrial land spanning Pawtucket and Central Falls. Today, the area is one of the most significant

IREM president’s message: Our new reality - Staying ahead of supply chain delays - by Yoany Vargas

Supply chain delays are slowing construction, ratcheting up operating costs, and extending turnover timelines across Greater Boston, directly reducing revenue and increasing the workload for multifamily and

Revitalized Town Centers: Retail??? - by Carol Todreas

It is now widely accepted that customers want to shop in person at physical stores. Brands know that they do better business in a physical store than just on line so they want to open stores. Demand for retail space by digital merchants, local entrepreneurs, and newly developed national chains