(1).png)

News:

Owners Developers & Managers

Posted: March 4, 2016

Question of the Month: Insatiable demand and limited construction - How is it affecting Boston’s multifamily market? - by Tim Thompson

Marcus & Millichap" width="170" height="212" /> Tim Thompson, Marcus & Millichap

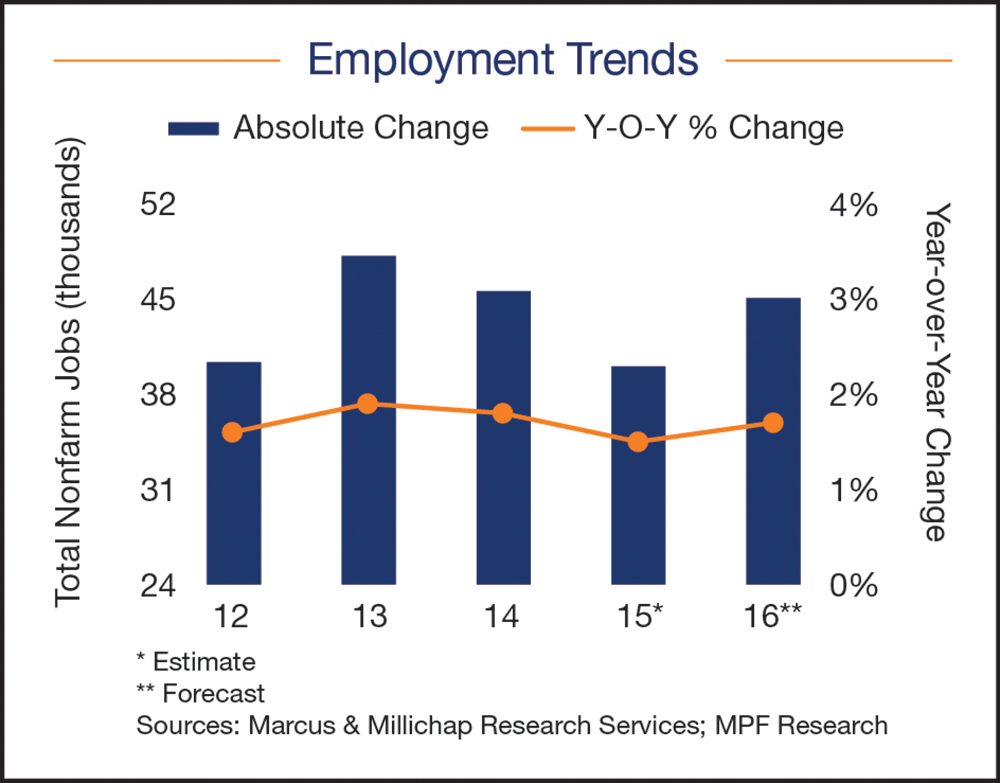

Marcus & Millichap" width="170" height="212" /> Tim Thompson, Marcus & MillichapStrong job growth and household formation coupled, with high multifamily demand and low multifamily vacancy, are the factors supporting Boston’s booming multifamily property market. Last year, employers created approximately 40,000 jobs with the majority of new positions in the professional and business services sectors boosting payrolls metrowide by 2.1%. The education, health services, government and hospitality sectors all reported significant payroll expansion. These employment gains aided the creation of 20,000 households in Boston in 2015, which prompted increased residential development.

This year, Boston employers will generate 55,000 positions metrowide, increasing headcounts by 2.1%. Tech companies expanding at Kendall Sq. include Google, which has grown its Cambridge Center campus. Additionally, General Electric plans to open its new headquarters in Boston in the first half of 2018. General Electric will hire approximately 200 workers for positions in software engineering. Given these strong employment and population trends, demand for rental units throughout Boston will be heightened in 2016.

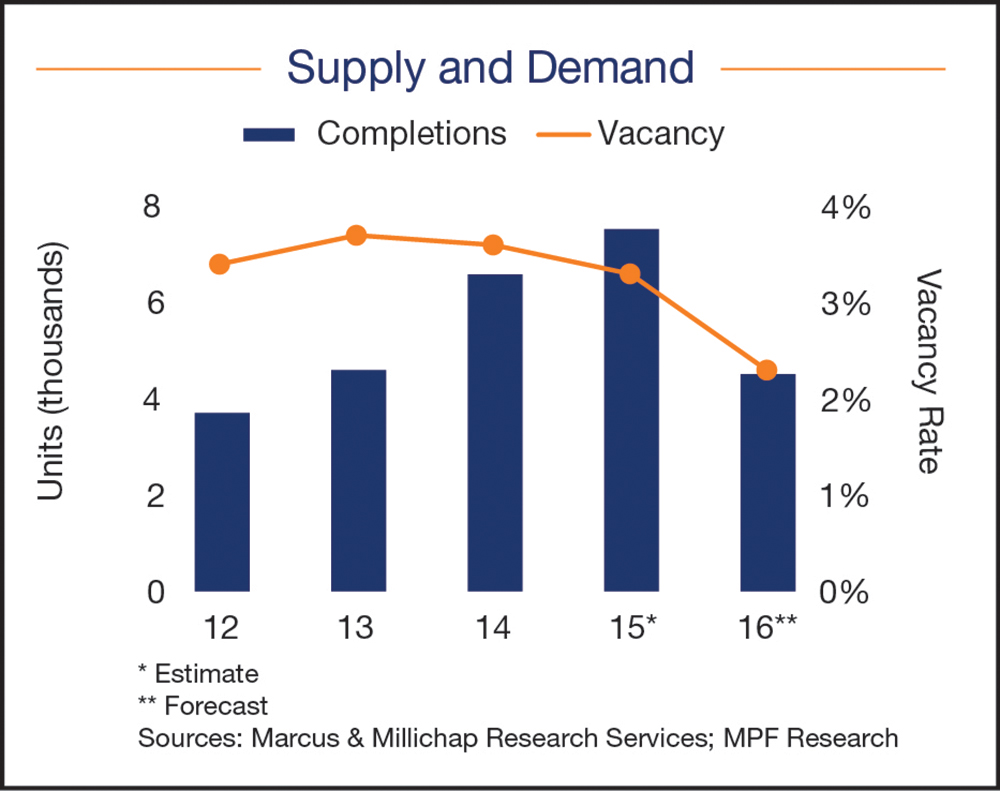

In 2015, Boston’s apartment tower boom altered the skyline of the core and surrounding areas, including the South End, Seaport District, Fenway and Cambridge. Builders focused on providing apartments to meet growing demand, as evidenced by the significant rise in multifamily permit issuances. Last year, 6,700 rentals were delivered, raising the local supply of apartments by 1.5%, and as of the third quarter of 2015, nearly 8,000 units were under construction metrowide, with dates of completion slated through mid-2017.

Another factor that kept demand for rental housing high last year was that the median household income fell short of the minimum level required to qualify for a traditional mortgage with a 20% down payment. As a result, many residents simply could not afford to purchase a home. This, along with a desire among new employees for a live-work-play environment, drove renter demand and will continue to do so in 2016.

In 2016, developers will complete 4,500 new units, increasing local stock by 1%. It is anticipated that those employed at nearby tech and bioscience firms will seek residences close to work and the amenities that areas within the Rte. 128 loop provide. While homeownership may finally become an option for some residents, the cost still remains out of reach for the majority of those employed in this area. Developers will continue to alter the local landscape of the Cambridge, Fenway, Seaport District and South End areas to meet tenant demand. Robust desire for new rentals with the latest amenities will support occupancy gains in core-based apartments, and will further reduce vacancy.

Though there was a heavy volume of construction in 2015, rental housing demand was insatiable and supported a decline in vacancy. The average vacancy in Boston shrank 80 basis points to 2.8% year-over-year on net absorption of nearly 10,000 apartments.

In 2016, steady absorption of new apartment stock, combined with a decelerating construction pipeline, will trim down vacancy more than last year. Given the projection for strong apartment demand this year, vacancy is expected to edge down 100 basis points to 1.8% as existing apartments will face little competition from new supply. For this reason, rents throughout Boston are projected to continue to rise.

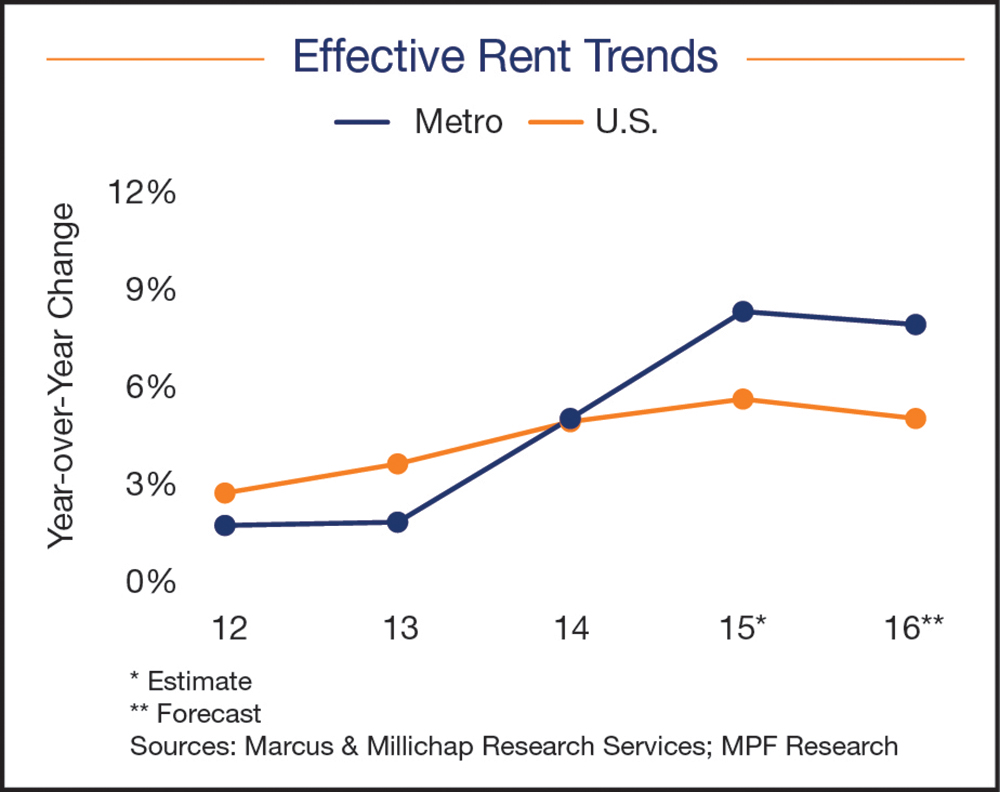

Last year, average effective rents advanced 2.8% metrowide, bolstered by employment gains, elevated household formation and the lease up of a large number of luxury units. For properties built since 2000, rents climbed 7.5% metrowide, which include properties in outlying areas such as Worcester.

In 2016, tight vacancy will support a 7.9% climb in average effective rent. Investors have noted the positive outlook for rent growth for multifamily properties in Boston, which will lead to strong continued investment activity.

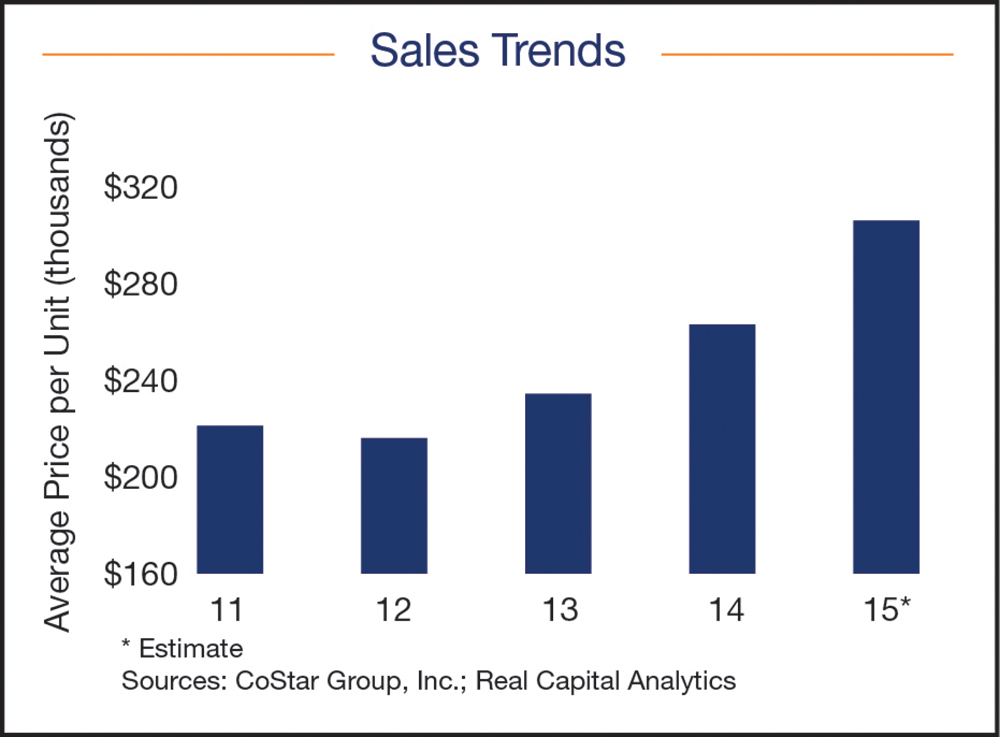

Last year, investors descended upon the Boston-area apartment market in search of the returns associated with tight vacancy and the stability of diverse rental demand drivers. The sales environment was characterized by few listings and intense competition from a large buyer pool that lifted values. As a result, cap rates began to level off overall, ranging from the sub-5% tranche for properties in the core and surrounding neighborhoods to the 7 to 8% range for assets in far outlying communities beyond I-495.

With respect to investor activity in Boston last year, institutions traded into newer, mixed-use properties downtown at initial yields in the sub-4% area. Concurrently, there was a rising tide of lower-tier multifamily trades which indicated that private investors in the area possessed a higher risk tolerance. Local buyers were responsible for the majority of transactions of value-add and lower-tier properties. Additionally, a large number of trades occurred in the North Shore and Merrimack Valley areas as capital was placed into class C assets, which represented a shift from prior periods.

In 2016, investors’ interest are expected to remain piqued, generating competition across all asset classes. Many investors will begin to look to class B and C properties both in the core and the surrounding areas, in search of higher first-year yields.

With the same fundamental factors in play that supported the multifamily rally last year, 2016 may well be another explosive year for Boston’s multifamily market.

Tim Thompson is sales manager at Marcus & Millichap, Boston, Mass.

MORE FROM Owners Developers & Managers

The Westin Portland Harborview to host exclusive VIP pop-up with The Woods Maine July 24–26

Portland, ME The Westin Portland Harborview will introduce an exclusive, limited-time pop-up shop with The Woods Maine, taking place July 24–26 in the city’s Arts District. This elevated retail experience brings The Woods Maine, the acclaimed Maine lifestyle brand behind the popular retail shop in Norway, Maine, directly to hotel guests and the local community.

Quick Hits

Columns and Thought Leadership

Revitalized Town Centers: Retail??? - by Carol Todreas

It is now widely accepted that customers want to shop in person at physical stores. Brands know that they do better business in a physical store than just on line so they want to open stores. Demand for retail space by digital merchants, local entrepreneurs, and newly developed national chains

IREM president’s message: Our new reality - Staying ahead of supply chain delays - by Yoany Vargas

Supply chain delays are slowing construction, ratcheting up operating costs, and extending turnover timelines across Greater Boston, directly reducing revenue and increasing the workload for multifamily and

Retail infill strategy to activate Pawtucket’s Conant Thread District - by Gaetan Kashala

Until recently, the Conant Thread District consisted of approximately 150 acres of underutilized industrial land spanning Pawtucket and Central Falls. Today, the area is one of the most significant

Florida ruling raises bar for condo terminations and buyouts - by Michael Karsch

On October 14, 2025, in a landmark decision with significant implications for the Florida real estate market, the Supreme Court of Florida formally denied Two Roads Development’s (TRD Biscayne LLC) petition for review in its long-running case against unit owners of Biscayne 21,