(1).gif)

News:

Finance

Posted: October 14, 2022

Residential market: Times are a changing! - by Marc Nadeau

The residential market in New England, and much of the country for that matter has seen the highest level of both activity and increases in prices in decades. The past two years have been somewhat blinding in terms of both pace and market appreciation. Relative to most residential markets in Connecticut, most have experienced double digit increases in prices year over year. We have also seen the shortest marketing times on record with many of the homes that came to market over the past two years selling over asking price.

The obvious elements that fed the market in Connecticut and other states were a combination of three things:

1. Record low-interest rates for borrowing.

2. New buyers entering the market.

3. A migration of buyers that initially came from metropolitan and urban cities, looking to move to areas of lesser density and escape COVID.

The not-so-obvious elements that drove the market upward were supply chain issues and the precipitous increases in the cost of building materials. Everything from lumber to roof shingles and toilet seats more than doubled in cost. That meant that anyone vying for a newly built house would be paying a great deal more. The same would be true for a recently renovated home, with those improvements, if they were contributory to modernizing, updating and enhancing an existing home would most certainly bring bigger dollars.

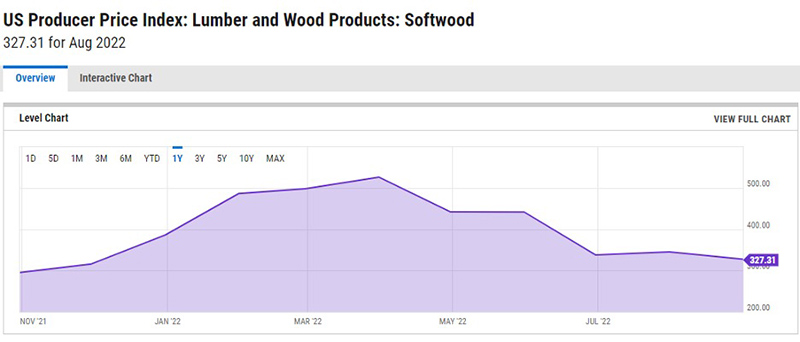

Lumber prices peaked in April of this year and are slowly coming down, but not to the levels of pre-COVID prices. Tracking the lumber market via the Producer Price Index revealed a decline of 5.16% for lumber and wood products over the past month (July to August of 2022) but, the year over year pricing is up 14.76%.

What to Expect in the Coming Year or Two

We have already seen the beginning of declining home prices and yes, values. The most recent statistics released by the National Association of Realtors indicated that the median price of a home in the U.S. in August was $389,500, down from $403,800 in July of the same year. This represents a decline of 3.5%.

A recent article published by the Financial Times in Britain indicated that the expected decline in home values would be in the area of 30% over the next two years.

Just as there were elements that drove the market upward in the past couple years, there are now elements that are driving it downward. This appraiser points to the following elements that are now driving the market:

1. A precipitous rise in mortgage and interest rates. The Federal Reserve has increased the Federal Funds Rate multiple times this year starting late March of 2022 when the first increase was instituted. This time last year, the Federal Funds Rate was .25%, today the Federal Funds Rate is 3.25%.

2. Correspondingly, mortgage rates have increased with fixed 30-year mortgages now approaching 7.0%.

3. Consumer debt is at record levels.

4. The equity markets have been roiling and we are now officially in a bear market. The S & P 500 is down approximately 21% since the start of the year.

Summary

Having experienced multiple market cycles over the past 40 years that included the run-up of real estate prices in the late 1980’s, only to have the market collapse in 1991. The dot-com bubble burst in 2002 led to an adjustment in market pricing. That was after the Nasdaq Composite Market Index rose 400% between 1995 and 2000, falling 78% from its peak in October of 2002. The run-up of debt and poorly curated mortgage-backed securities resulted in a market crash in late 2008. Today, we have record debt, wages that have not kept pace with inflation, which by the way has been raging at an annual rate close to 10% over the past two years, higher mortgage rates, the metaphorical divining rod that is pointing to lower values.

If the past is any barometer, I would expect to see market declines in the range of 10% to 12% over the next year or two. After all, we couldn’t expect the soaring real estate market to continue, could we?

Marc Nadeau, SRA, is a certified general appraiser and president of the Connecticut Chapter of the Appraisal Institute.

MORE FROM Finance

Project of the Month: DeLucia and De Lise completing a $10m investment at 967 Elm St. in Manchester NH known as Rendezvous on Elm

Manchester, NH Most multifamily renovations start with a standard stack: a few floor plans that are copy/pasted up multiple floors. Rendezvous on Elm began somewhere else entirely. 27 residences, 27 different floor plans, and a $10 million project built around the idea that a boutique building should feel boutique, from each angle and for every resident.

(1).gif)

Columns and Thought Leadership

Are appraisers on the same page as the assessor? - by Richard Seman

The purpose of this article is to address problematic or confusing issues which may help assessors and appraisers to better understand how to value real estate for tax assessment purposes.

Massachusetts real estate transfers over $1 million face new tax rules as of November 1st - by Daniel Meyer

Attention to owners of real estate in the Commonwealth (and the title companies and other professionals who advise them), the Massachusetts Department of Revenue (the “DOR”) recently adopted a new “millionaire’s tax” via 830 CMR 62B.2.4

The focus on price per s/f compared to the comparable sales used in the appraisal report - by Dennis Chanski

Over the past several weeks, I have completed appraisal assignments for private clients. Interestingly, after submitting these appraisals, I received several phone calls – not to question the value, content, or any incorrect information, but rather to discuss the price per s/f compared to the comparable sales used in the report.

Reverse exchanges and the challenges of a competitive real estate market - by Michele Fitzpatrick

Our current, highly competitive real estate market poses specific challenges for investors who are considering taking advantage of a tax-deferred 1031 exchange. In this market, investors will have no problem selling their current property if priced properly, but they may find it difficult to find a suitable replacement property