News:

Brokerage

Posted: March 25, 2016

The value of Mom & Pop tenants should be assessed more carefully - by Michael Branton

Michael Branton, KeyPoint Partners

Michael Branton, KeyPoint PartnersIt began in a small health food store in Austin, Texas; a sporting goods store in New York City; and a general store in Arkansas. While the names may be different, many powerhouses in retailing today have their origins in the “Mom & Pop” stores of yesteryear.

And yet, in today’s retail environment, Mom & Pop stores are often overlooked - and perhaps under-appreciated - by retail landlords. The reasons why could be debated endlessly, but one can make a strong case that the value of Mom & Pop stores should be assessed more carefully. After all, a long time ago, the three retailers mentioned above, better known as Whole Foods, Abercrombie & Fitch and Wal-Mart, were not the retail aristocracy that they are today.

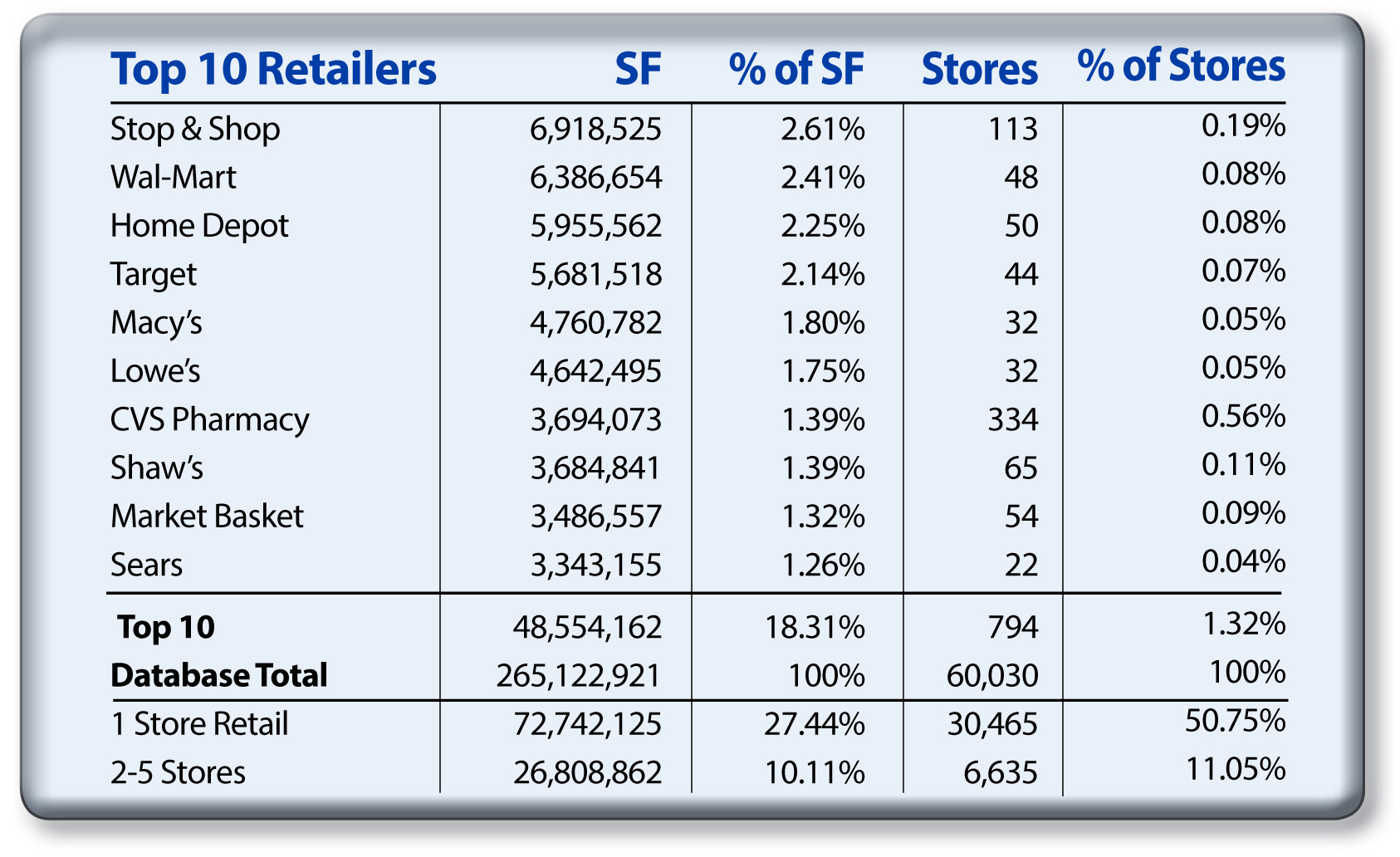

At KeyPoint Partners, we maintain a database, of more than 265 million s/f of retail space encompassing 60,000 storefronts and more than 33,000 unique tenants in Eastern Massachusetts, Southern New Hampshire and Greater Hartford - our unique, proprietary GRIID. According to the most current GRIID data, the top 10 retail tenants by square footage occupy 18.3% of the total retail space of the market, but only 1.3% of the total storefronts.

On the other hand, Mom & Pop stores (defined for this purpose as those operating one store and not affiliated with a larger chain or franchise) occupy 30,465 storefronts and 27.4% of the retail space within these three regions and a whopping 50.7% of all retail storefronts. The table below outlines the top ten retailers in the GRIID database by square footage and number of storefronts, compared with single-store retailers:

Mom & Pop stores are unquestionably the largest segment of the GRIID database, while smaller, multi-store retailers operating two to five stores constitute only 11% of all retail stores. As a result, Mom & Pop stores have a dramatic impact on a host of salient retail real estate issues such as vacancy rates, rental income, and property valuations.

Apart from sheer numbers, these one-of-a-kind retailers can add value to a property by enhancing the quality of a center. By their very nature, Mom & Pop stores create uniqueness, are constantly re-defining their originality, deliver a high quality customer experience to shoppers, and create diversity within the tenant mix. Mom & Pop stores often occupy second-generation spaces, and often, the most challenging spaces in shopping centers.

Furthermore, from a leasing standpoint, negotiations with Mom & Pop retailers are often simpler, less capital-intensive, and typically less protracted. An independent retailer’s decision to open (or close) stores is not tied to Wall Street, not dependent upon chainwide performance, and not linked to anything other than the merchant’s own ambition and availability of capital.

Landlords, brokers, and developers should take advantage of the opportunity to support local businesses, and enhance shoppers’ experience of their centers, by cultivating relationships with Mom & Pop stores. This year, when looking at merchandising plans and vacancies within your portfolio, why not consider the significance of Mom & Pop stores. Perhaps you can be the one to provide them with the opportunity of becoming the retail leaders – the Whole Foods, Abercrombie & Fitches, and Wal-Marts - of tomorrow.

Michael Branton is a senior associate with KeyPoint Partners, Burlington, Mass.

MORE FROM Brokerage

Horvath & Tremblay sells three retail properties in New Hampshire for $6.285 million

Franklin, NH Horvath & Tremblay has completed the sale of three retail properties in New Hampshire for a total of $6.285 million. Jake Mabardy, Aaron Huntley and Brad Canova of Horvath & Tremblay have completed the sale of Franklin Shopping Center. Horvath & Tremblay exclusively represented the seller and sourced the buyer to complete the transaction at a sale price of $3.595 million.

Quick Hits

Columns and Thought Leadership

The rise of AI in CRE - And what it means for every skilled profession - A broker & appraiser weighs in - by Bryan Plourde

This may seem self-serving, and I’ll be the first to admit it. But unlike some of the artificial intelligence tools now reshaping our industry, I am fully aware of my own bias. So, hear me out. The rise of AI in commercial real estate is not a distant threat or a speculative headline.

End of the year retail thoughts - by Carol Todreas

Now what? As the year comes to a close, the state of retail is always in the news. The answers vary greatly depending on who in the various related industries you ask, each offering a unique lens on the challenges and opportunities ahead.