News:

Spotlight Content

Posted: March 29, 2019

Top reasons for borrowers to lock in rates in early 2019 - by Michael Chase

NorthMarq

The start of 2019 has once again presented borrowers with an opportunity to take advantage of commercial mortgage rates near historic lows. As we make our way towards the end of the first quarter, here are the top reasons borrowers should be looking to lock in rates now.

Treasury Yields Remain Near Historic Lows

After hitting a 52 week high of 3.26% on October 9, 2018, the yield on the 10-year United States treasury steadily declined reaching a new 52 week low of 2.53%, as of this writing, on March 20, 2019. Remarks from Federal Reserve chairman, Jerome Powell, help to spur this latest drop. Chairman Powell commented that the Federal Open Markets Committee (FOMC) was unlikely to make further rate increases for the remainder of 2019. His remarks also included confirmation the Federal Reserve would begin reducing efforts to shrink its balance sheet. A dovish stance from the FOMC along with a reduced supply of securities in the market are likely to help keep treasury rates from rising.

Until recently, the Federal Reserve was primarily concerned with inflationary pressures within the United States. As a result, they made four rate increases over the course of 2018. These actions led to a rise in short-term rates with little corresponding movement from long-term rates. This was partially due to market concerns of a future economic downturn, but it was also because yields for competing sovereign debt remained depressed. On March 8, 2019, the 10-year German bond yield reached 0.05%, its lowest level since 2016. Meanwhile, the 10-year Japanese bond yield is currently offering a negative 0.035%. While yields for United States treasuries remain historically low, they continue to attract demand from foreign capital seeking yields that are relatively high when compared globally.

Reduced Corporate Bond Yields

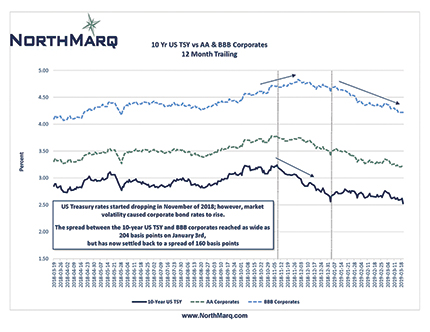

When trying to determine where commercial mortgage rates are headed, it is helpful to not only look at treasury yields, but also at possible alternative investments for lenders. For commercial mortgages the most common alternative investment is typically BBB corporate bonds. At the end of 2018, volatility in the corporate bond market caused yields to widen. Many borrowers wondered why they were seeing higher commercial mortgage rates even as treasury yields were declining. From early November to January 3rd the spread between treasuries and BBB corporate bonds widened from 150 basis points (bps) to 204 bps. As a result, lenders seeking relative value had to quote higher commercial mortgage rates. As 2019 has progressed, the corporate bond market as settled down, and the spread between corporate bonds and treasuries is back down to around 160 bps. This has allowed lenders to quote tighter mortgage spreads and borrowers to lock in lower commercial mortgage rates.

Opportunity for Reduced Prepayment Penalties

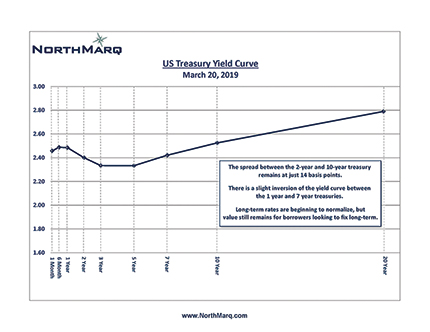

In addition to long-term rates remaining low, the overall yield curve is providing a rare opportunity for borrowers in the current market cycle. As mentioned earlier, the FOMC made four rate increases throughout 2018 pushing up short-term rates while long-term rates remained low. In fact, there is currently an inversion in the yield curve between the 1-year and 7-year treasuries.

Borrowers who may have been stuck with high prepayment penalties in prior market cycles may be able to benefit now. In particular, many borrowers with loans from banks subject to SWAP breakage are now finding themselves “in the money” and able to pay their loans off at a reduced principal balance instead of a prepayment penalty.

Lots of Capital Chasing Deals

There is still plenty of capital chasing after good transactions. The majority of lenders still have availability in their allocations for 2019; however, as the year goes on, some lenders who were successful in achieving their volume goals may become less aggressive. There are several options available for borrowers seeking to lock a rate today even for a closing later this year. Those who act now can still take advantage of a competitive landscape.

How long will the Federal Reserve maintain their dovish stance? What will happen to rates if a trade agreement between China and the United States is finalized, or if Brexit is resolved? How will the corporate bond market react to low treasury yields? How long before lenders fill their volume targets for 2019? Answers to any of these questions will have an impact on mortgage rates going forward. Borrowers who were waiting to time the market currently have a lot going their favor and are in a great position at the start of 2019.

Michael Chase is a managing director of NorthMarq, Boston, Mass.

Tags:

Spotlight Content

MORE FROM Spotlight Content

Participation opportunities for our Industrial Review 2026

The New England Real Estate Journal is pleased to announce participation opportunities for our upcoming Industrial Review 2026, a special publication highlighting the people, projects and properties shaping New England’s industrial real estate market.

(1).gif)

Columns and Thought Leadership

How do we manage our businesses in a climate of uncertainty? - by David O'Sullivan

These are uncertain times for the home building industry. We have the threat of tariffs mixed with high interest rates and lenders nervous about the market. Every professional, whether builder, broker, or architect, asks themselves, how do we manage our business in today’s climate? We all strive not just to succeed, but

As legacy names recalibrate, new entrants are moving in with fresh capital, new technologies, and business models tailored to today’s supply-chain needs - by Michael Harrington

Southern New Hampshire’s industrial market has always punched above its weight. For decades, the region has attracted a mix of advanced manufacturing, beverage and food producers, logistics operators, and specialty

Limited supply fuels landlord‑friendly conditions in Rhode Island’s industrial market - by Julie Freshman and George Paskalis

As we enter the spring of 2026, the Rhode Island industrial real estate market stands on stable footing, following several years of resilience fueled by constrained supply, steady demand, and dynamic economic conditions.

Shallow-bay wins on 495/128: A renewal-driven market with a thin pipeline - by Nate Nickerson

The Boston industrial market entered mid-2025 in a bifurcated state. Large-block vacancy remains elevated, while shallow-bay along the 495/128 corridor continues to prove resilient. Fieldstone’s focus on this geography positions us squarely in the middle of a renewal-driven, supply-constrained