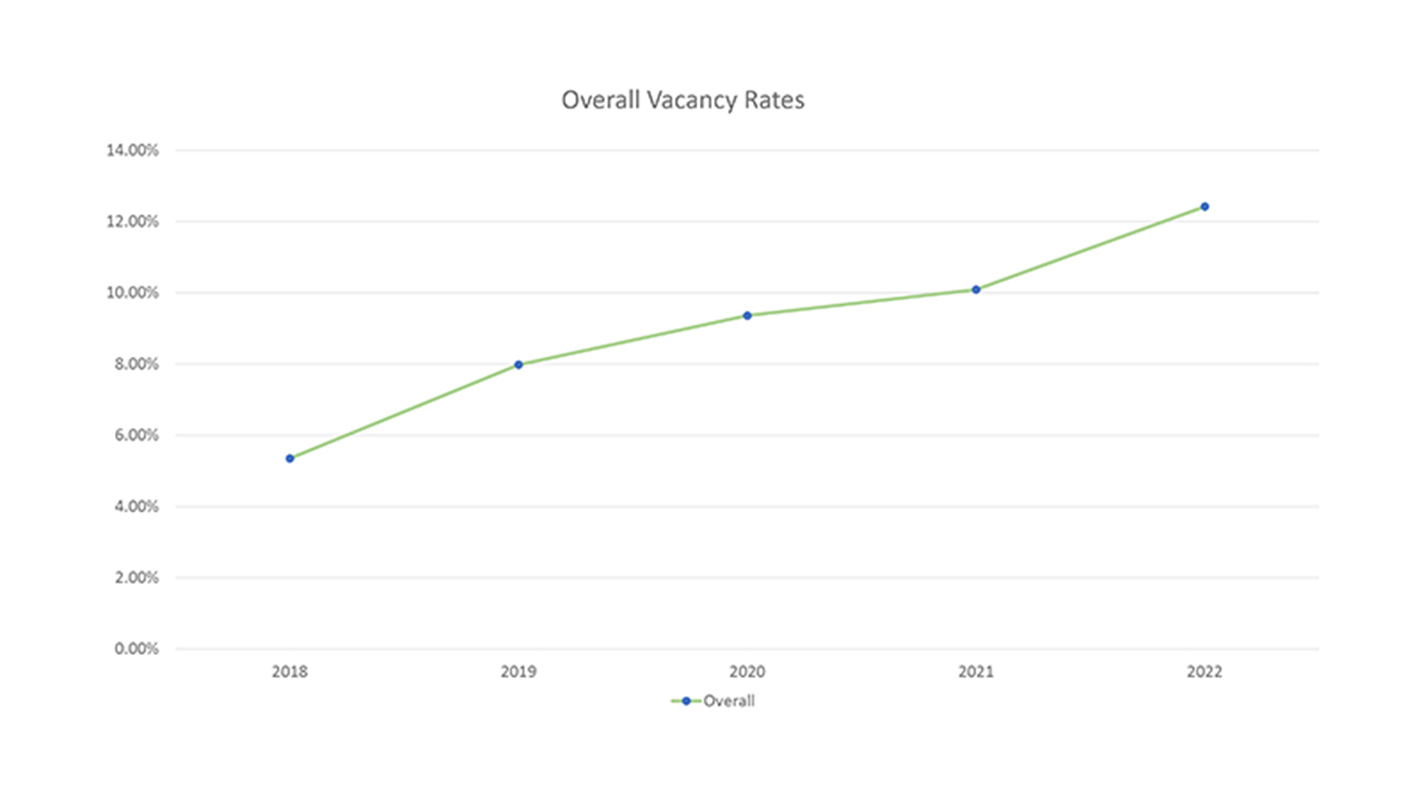

When you look at the overall office market in Greater Portland for 2022, the sector was in transition. Another year removed from COVID, and another year, where we still do not believe we have seen the last of its impacts. Firms are still trying to determine how many of their employees will be returning to the office and therefore how much space they will need. Some firms are planning for 40 – 50% of their FTE to be in the office on any given day (Travelers, LogistiCare, Prudential, UBS), others have decided to vacate the market entirely and consolidating offices in other New England states (Harvard Pilgrim, United Healthcare), while others are keeping the same amount of space or growing (Woodard & Curran, Capital One, Ameriprise). We expect this transition to balance out over the next 12-18 more months.

Outside of corporate America, small local users continue to dominate the majority of transaction volume. Of the 165 deals done in 2022, 93% were for 10,000 s/f or less, which is consistent with our historical market data. Interestingly, we also saw a 14% increase in the number of transactions made in the office market YOY.

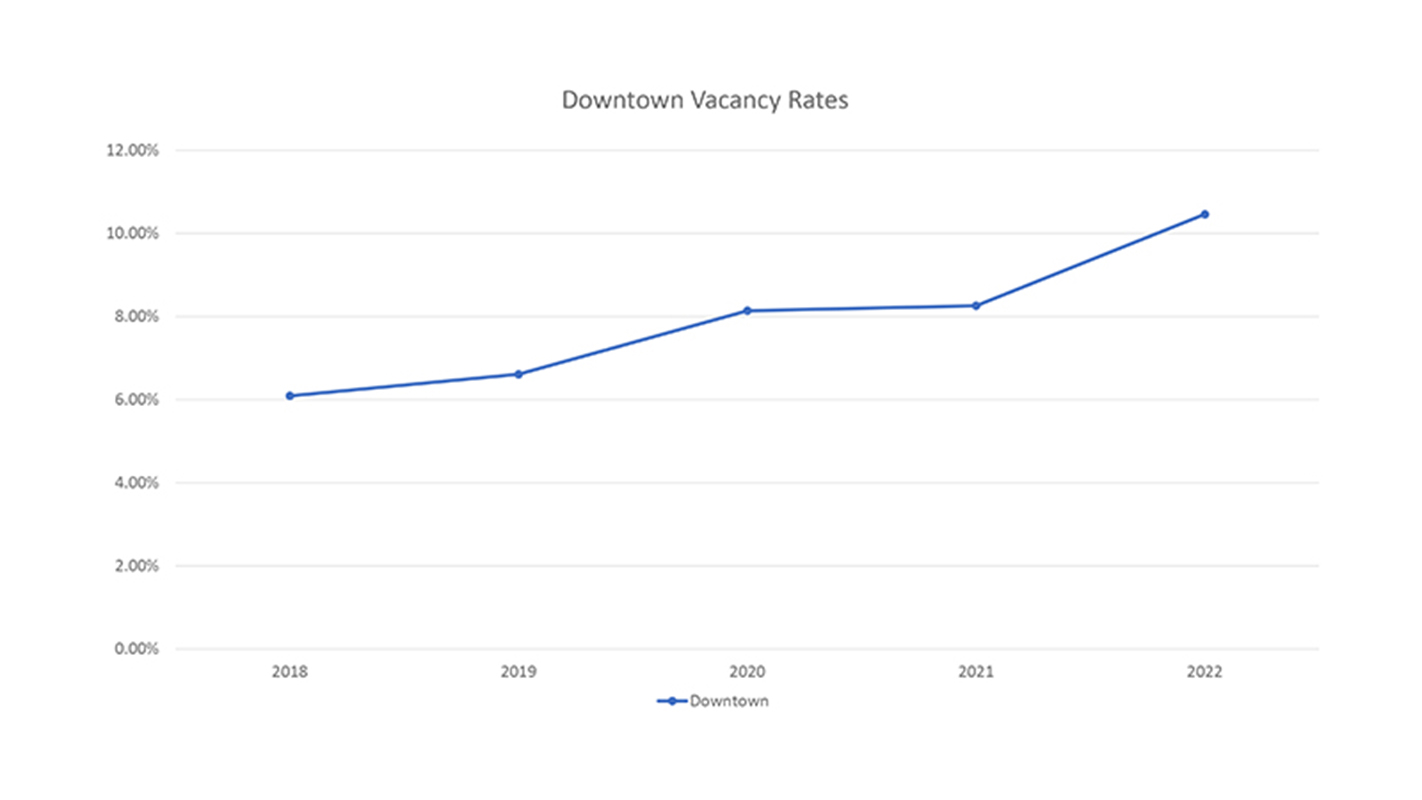

DOWNTOWN MARKET

The downtown market class A sector was the most resilient with overall vacancy dropping slightly from 9.09% to 8.92%. Class A saw a positive absorption of 212,000 s/f driven by 12 Mountfort St. (129,866 s/f) and 110 Thames St. (90,000 s/f) coming online this year 100% leased. 12 Mountfort St. was built for Covetrus, who subsequently subleased 56,000 s/f to Woodard & Curran.

Downtown class B overall vacancy increased significantly from 7.83% to 11.42%, resulting in a negative absorption of 313,000 s/f.

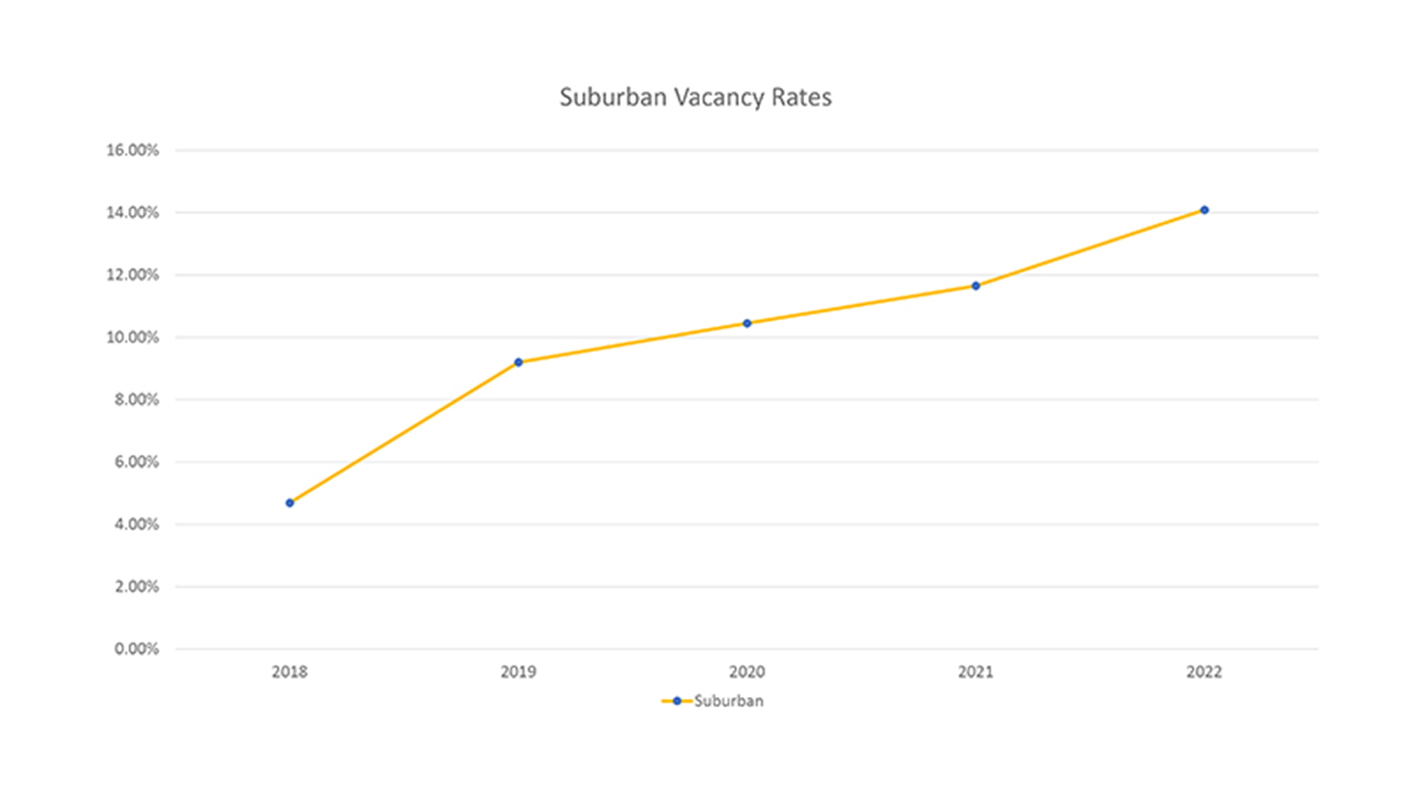

SUBURBAN MARKET

The market is a buzz with the amount of vacant space in the suburban office market these days - with overall vacancy increasing from 11.63% to 14.09%. With a large amount of corporate, cubicle-type space we saw come on the sublease market in 2021, it was only a matter of time before this square footage hit the direct vacancy rate. Interestingly enough, the majority of this space is in the Maine Mall sub-market. We expect to see the sublease spaces roll over to an increasing direct vacancy rate over the next few years.

FORECAST

As the pandemic comes to an end and the world gets back to normal, corporate America will find the equilibrium of work from home vs in the office. Most senior executives would prefer employees to be in the office, promoting employee camaraderie and mentoring, therefore we expect more employees will be coming back to the office over the next 12 to 18 months increasing the need for larger office space.

No bold or surprising predictions here, we expect to see more of the same continue in the next twelve months. The downtown market will remain steady overall, and the suburban market will be in flux, with higher vacancies and more space on the sublease market. One thing for certain, we expect to see landlords in both the downtown and suburbs look more closely at conversion possibilities as tenants have shifted into the driver’s seat and demand has slowed.

Jim Harnden is a partner/broker and Sam LeGeyt is a broker on the industrial team both with The Dunham Group, Portland, ME.

.png)